Q1 2026: Uncompensated Risk

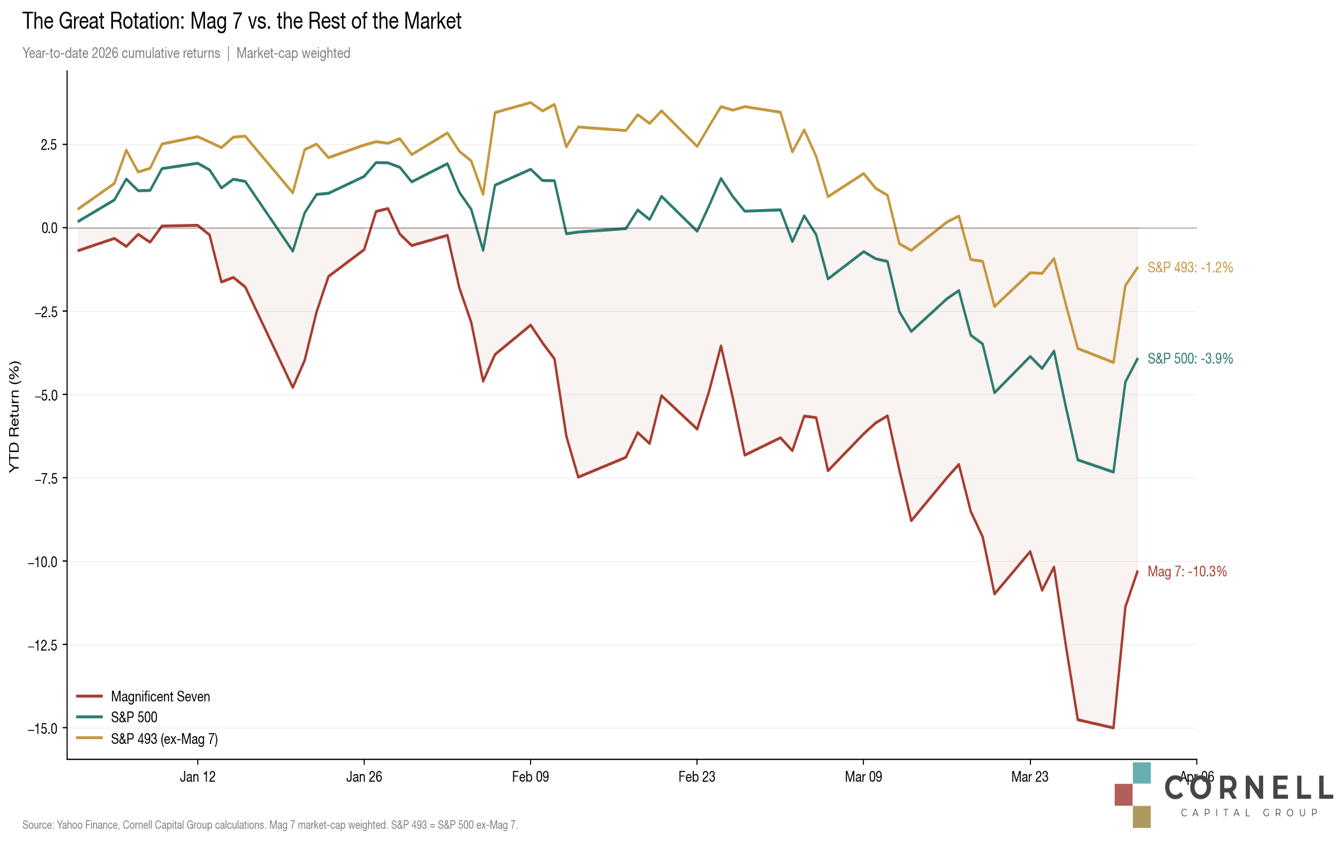

The S&P 500 fell 3.9% in Q1, dragged lower by a 10.3% decline in the Magnificent Seven. With the equity risk premium near historic lows, investors are accepting equity volatility for very little compensation above risk-free rates.

Key Points

- The S&P 500 fell 3.9% in Q1, dragged lower by a 10.3% decline in the Magnificent Seven. The quarter was marked by sharp rotations, geopolitical shocks, and elevated volatility.

- At current valuations, even modest surprises produce outsized consequences — as the Iran conflict demonstrated.

- The equity risk premium remains inadequate. Investors are accepting equity volatility for very little compensation above risk-free rates.

- Structural risks remain — AI capital intensity, fiscal sustainability, passive unwind, geopolitical uncertainty.

Q1 2026 Market Performance

The first quarter of 2026 was marked by a sharp shift in market tone — from the steady, liquidity-driven advance of recent years to a far more turbulent and policy-sensitive environment. Renewed uncertainty around tariffs, trade policy, and fiscal direction injected volatility into both equities and rates, while geopolitical tensions — notably the continuing war in Ukraine and the eruption of conflict in Iran — added further risk through energy markets and global supply chains.

The weakness in the headline indices masks a more concentrated dynamic: the market’s decline has been driven disproportionately by the unwinding of the “Mag 7” — mega-cap technology leaders that had previously powered the bulk of index returns. As these stocks have pulled back — reflecting valuation sensitivity, rising capital intensity around AI, and policy uncertainty — their sheer weight in the indices has dragged the overall market lower. Overall, the S&P 500 fell 3.9%, pulled down by the Mag 7’s collective 10.3% decline. Beneath the surface, however, many sectors proved far more resilient: energy rose 36.5% in response to the oil shock associated with the Iran war, underscoring that this is less a traditional bear market and more a repricing of leadership at the top of the market.

The Equity Risk Premium: Is There Adequate Compensation?

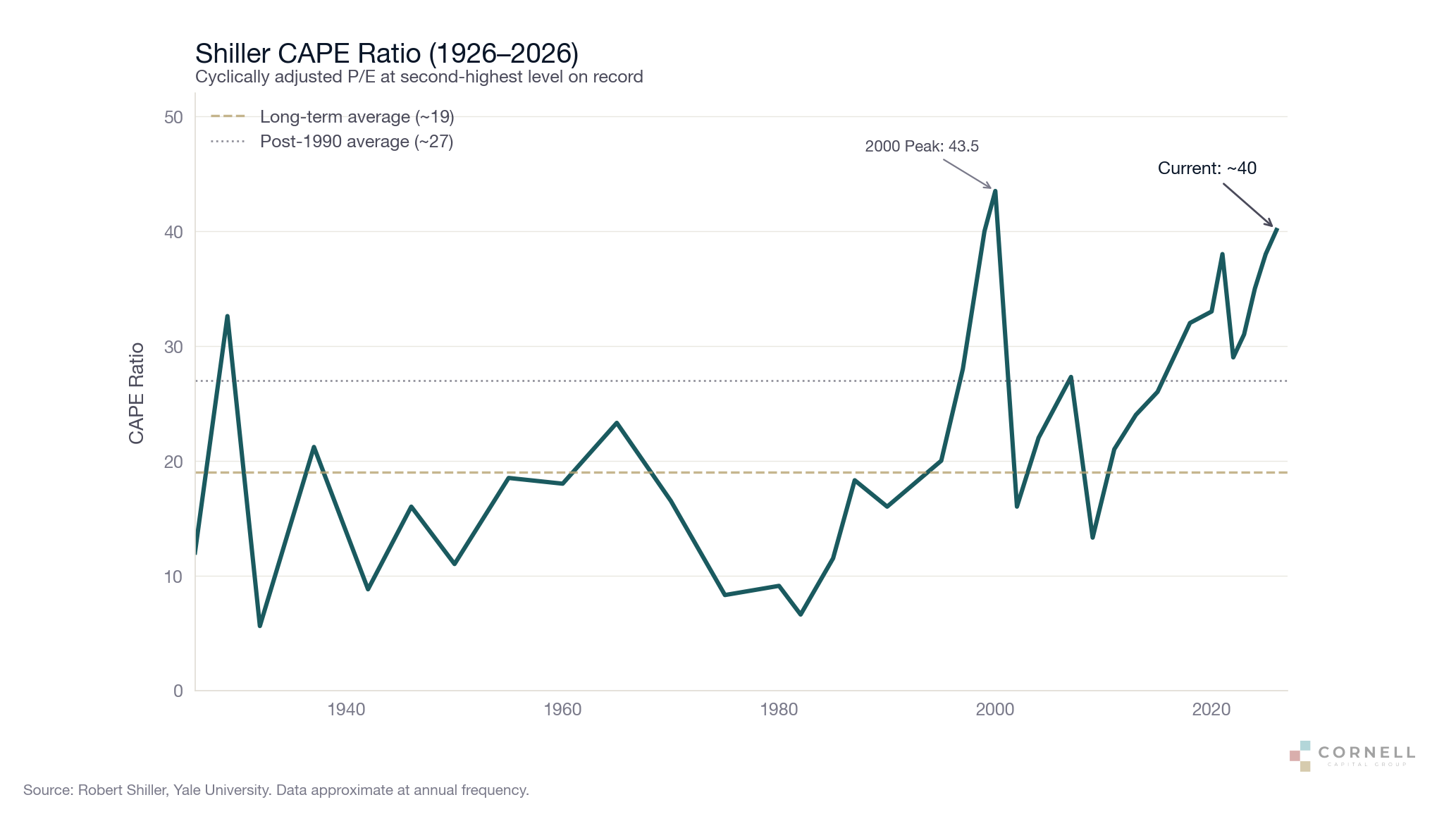

In a previous commentary, we argued that the equity risk premium had structurally declined — reflecting better regulation, improved monetary policy, and the demonstrated willingness of governments to backstop crises. That argument still holds. But there is a difference between a lower risk premium and an inadequate one. As of early 2026, the S&P 500 traded at a Shiller CAPE near 40 — among the highest levels in history.

Using Aswath Damodaran’s framework, the implied equity risk premium has compressed to levels reminiscent of the late 1990s. Investors are accepting equity risk with almost no margin for error.

The Iran conflict has made this inadequacy visceral. Since U.S. and Israeli strikes on Iranian nuclear and military facilities began in early March, Brent crude surged past $100 per barrel for the first time since 2022, briefly touching $126 as Iran’s closure of the Strait of Hormuz disrupted a fifth of global oil supply. The S&P 500 fell more than 5% in March alone, the VIX spiked from 16 to above 31, and the Nasdaq entered correction territory. The threat of sustained higher oil prices feeding into headline inflation pushed expectations for the first Fed rate cut well into the second half of the year. This is precisely the kind of environment in which investors should demand a generous equity risk premium, yet the premium they entered the year with was razor thin. The Iran war did not create a new risk so much as it exposed the fragility of a market priced for a benign world that never existed.

The quarter’s final days illustrated the other side of this volatility. As reports emerged of back-channel negotiations in Oman and signals from Iran’s president of a willingness to end hostilities, the S&P 500 surged 2.9% on March 31 — its best single session since May. The speed of the reversal underscored how much geopolitical risk had been priced into equities and how quickly sentiment can swing when the risk premium is thin. Whether these diplomatic signals lead to a durable resolution remains uncertain, but the episode reinforced a central theme of this quarter: in a market priced for perfection, even the possibility of relief produces outsized moves.

The Arithmetic of Low Premiums

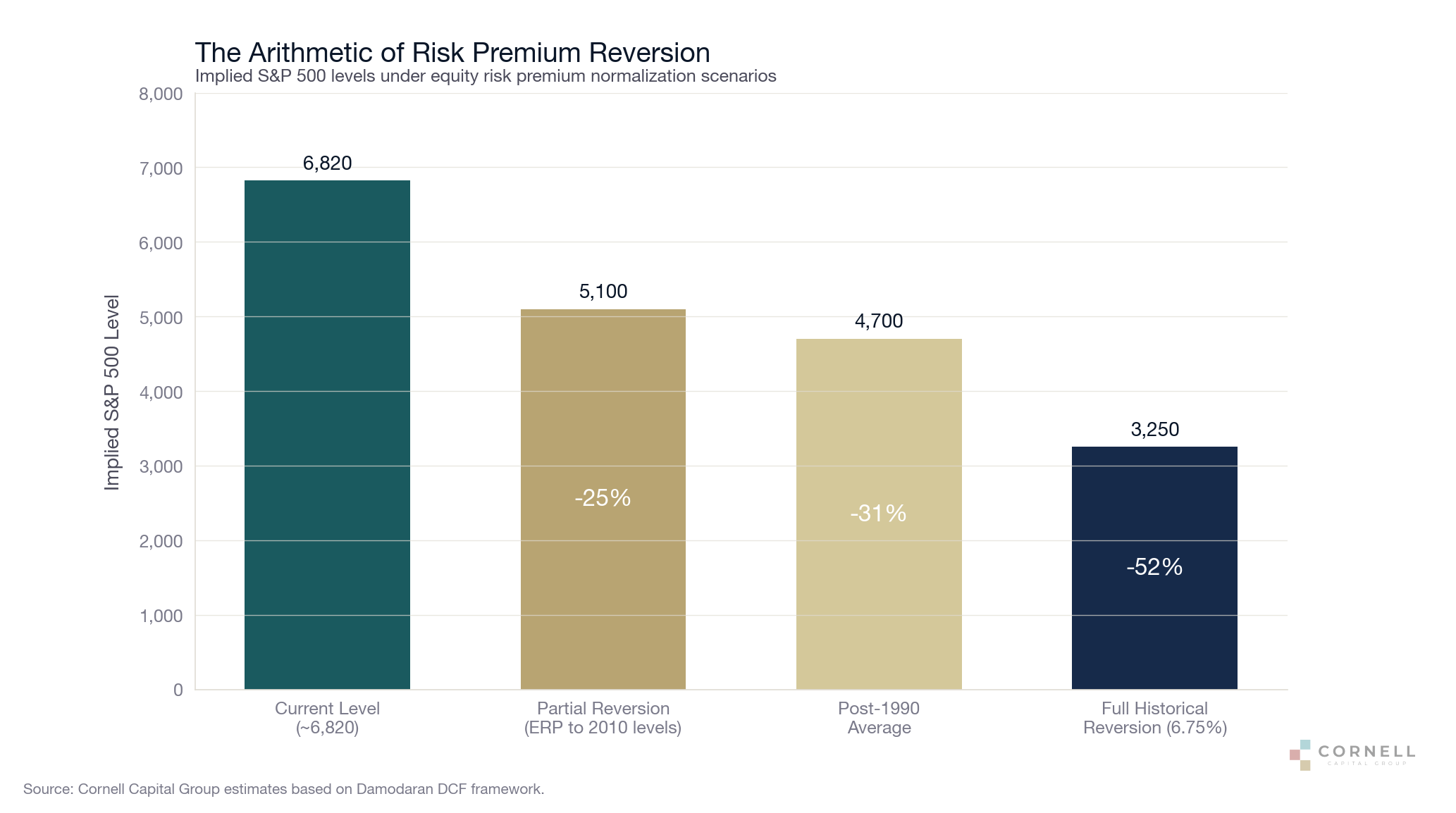

If today’s compressed premium persists, and earnings grow roughly in line with nominal GDP, expected equity returns over the next decade are likely in the 4–6% range. That is not meaningfully higher than what high-quality bonds currently offer — despite equities carrying substantially greater volatility and drawdown risk. If, however, the risk premium rises even modestly toward more normal levels, the adjustment must come through prices. A partial reversion — say, back to levels seen as recently as 2010 — would likely require a 25–30% decline in the S&P 500.

The asymmetry is the key point. When the risk premium is already thin, upside is limited by the return you are not being paid, while downside is magnified by the absence of a valuation cushion. With the 10-year Treasury yielding 4.35% and investment-grade corporates offering roughly 5.0%, fixed income increasingly competes with equities on a risk-adjusted basis — particularly for investors who do not need to bear full equity risk.

Structural Risks

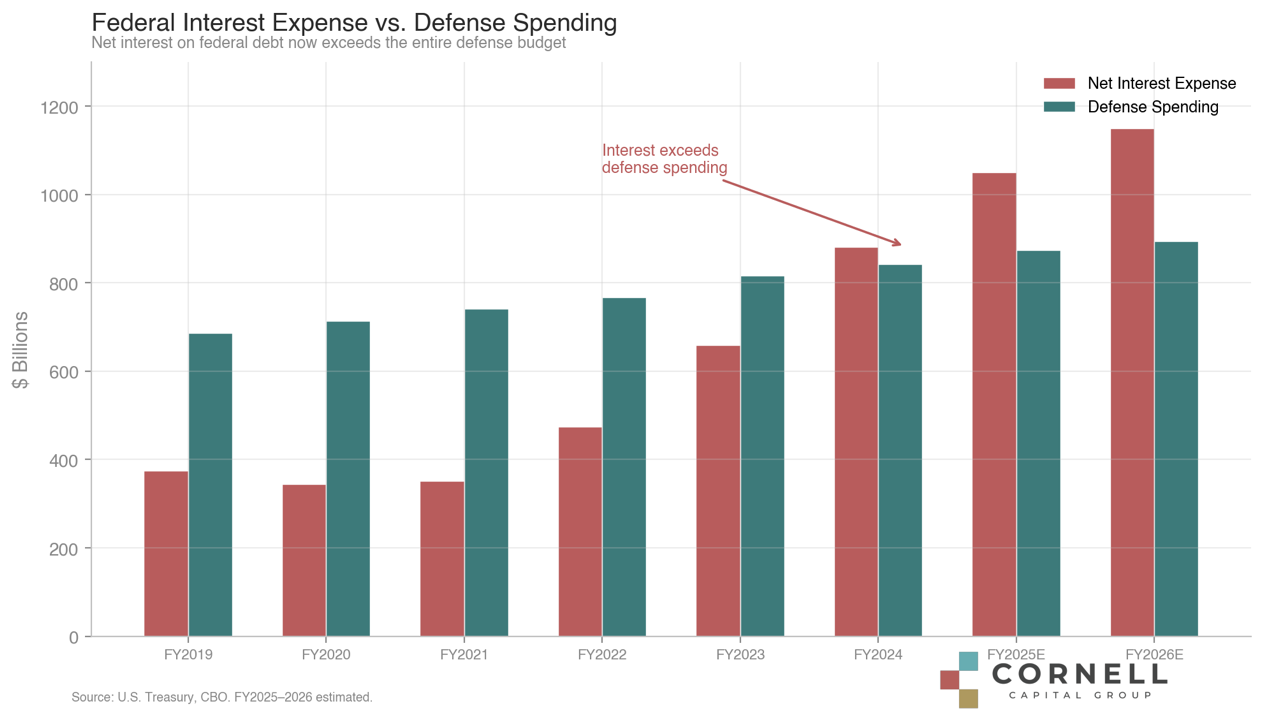

The federal government’s fiscal position continues to deteriorate. The CBO projects a $1.9 trillion deficit in fiscal 2026, with federal debt at 101% of GDP and net interest payments reaching $1 trillion annually — exceeding the entire defense budget. As we have argued in previous memos, persistent fiscal deficits have acted as a powerful tailwind for corporate earnings and stock prices, but ever-rising government debt brings with it higher interest costs and growing refinancing risk. At some point, the bond market may demand a higher price for absorbing that supply, which would mechanically compress equity valuations.

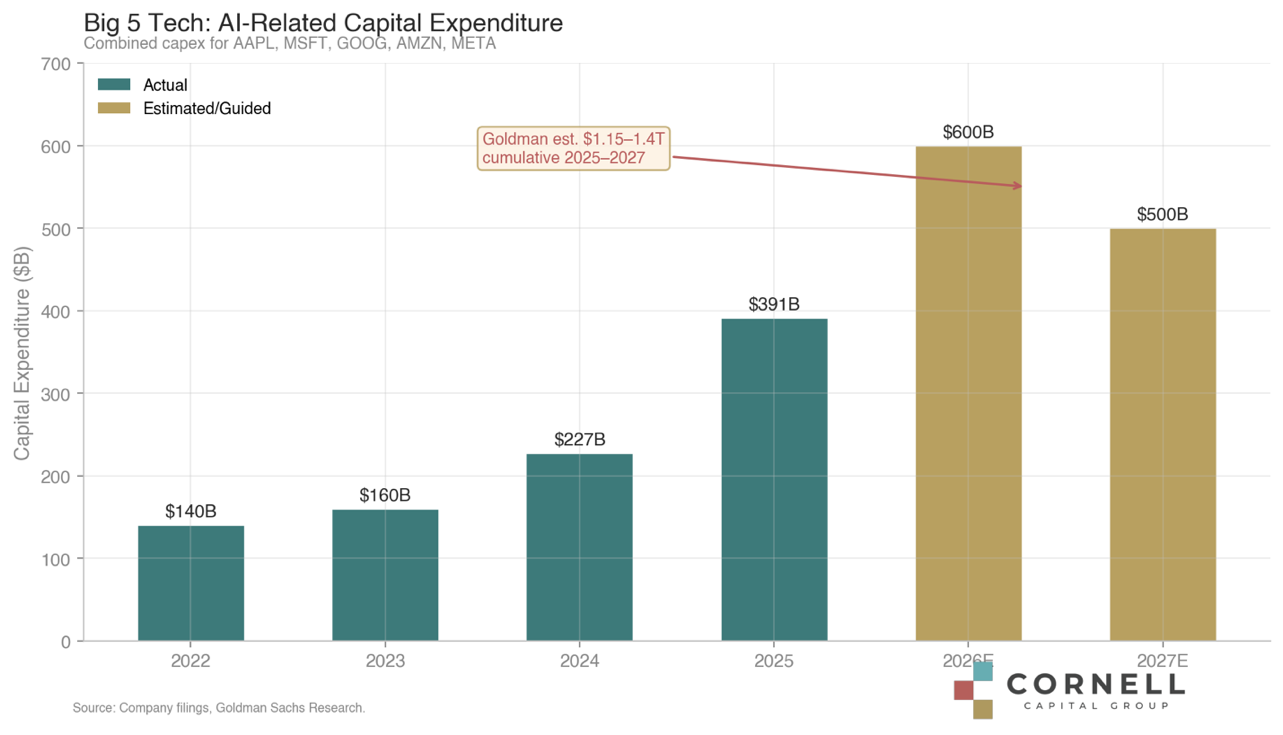

Meanwhile, the trajectory of AI capital spending remains a first-order risk to the mega-cap stocks that dominate the index. The five largest U.S. tech companies increased capex from roughly $227 billion in 2024 to $391 billion in 2025, with guidance pointing toward more than $600 billion in 2026. Each firm feels it must invest to avoid falling behind, but when all invest simultaneously the likely outcome is margin compression rather than durable competitive advantage. History — from fiber optics in the 1990s to railroads before that — suggests that transformative infrastructure often creates enormous social value while destroying investor capital. For a more detailed analysis, see our companion publication on this topic: The AI Prisoner’s Dilemma.

Investment Implications

None of this requires investors to sell everything and move to cash. But it does have practical implications.

Revise return expectations downward. Investors planning around historical equity returns of 8–10% per year are likely to be disappointed. Stress-test assumptions against a lower-return environment.

Diversification matters more, not less. When the risk premium is thin, the penalty for concentration in high CAPE countries could be severe. Most global markets trade at CAPE ratios between 16 and 22 — offering materially more attractive entry points than U.S. large-cap equities and providing risk-reducing diversification.

Consider the alternatives. With high-quality bonds offering yields competitive with expected equity returns at a fraction of the volatility, the opportunity cost of a more conservative allocation has declined meaningfully. This does not mean abandoning equities — it means ensuring that every dollar of equity exposure is earning its keep.

Conclusion

The equity risk premium is not a forecast — it is a price. It tells you what you are being paid to bear uncertainty. Right now, that price is telling investors they are accepting high equity market volatility for little additional compensation above what risk-free assets provide. You do not need to predict the future to find this troubling. You simply need to acknowledge that the future is uncertain and ask whether the return you are receiving reflects that uncertainty. At current levels, our conclusion is that it does not.

As always, our approach remains grounded in comparing price with value. The exceptional returns of the post-crisis era were driven by forces — expanding profit margins, falling risk premiums, persistent fiscal stimulus — that are now largely exhausted. The environment ahead calls for discipline, diversification, and a clear-eyed assessment of the compensation being offered for the risks being borne.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction.