Another Covid Victim Short Termism

Download PDF Key Points S&P 500 returns (954.5%) following the 2008 Global Financial Crisis…

In a famous editorial published in the Wall Street Journal, Warren Buffett and Jamie Dimon, the chairmen of Berkshire Hathaway and JP Morgan respectively, took the stock market to task for being too short-term oriented. The authors state that “ This announcement today builds on the Commonsense Corporate Governance Principles that business leaders developed in 2016. These principles acknowledge that the financial markets have become too focused on the short term.”This view is widely held by many corporate executives who claim that the short-term orientation of the market with its on the next quarter, or at most the next year, makes it difficult for them to plan appropriately for the long term. In the past, we at Cornell Capital Group have argued that there is a good deal of market evidence which contradicts this view, but the recent Covid crisis has been the coup de gras. In our view, Covid has killed short-termism once and for all. The behavior of the stock market during a year of Covid induced earnings declines is the final death knell for the hypothesis that the market is infected with short-termism.

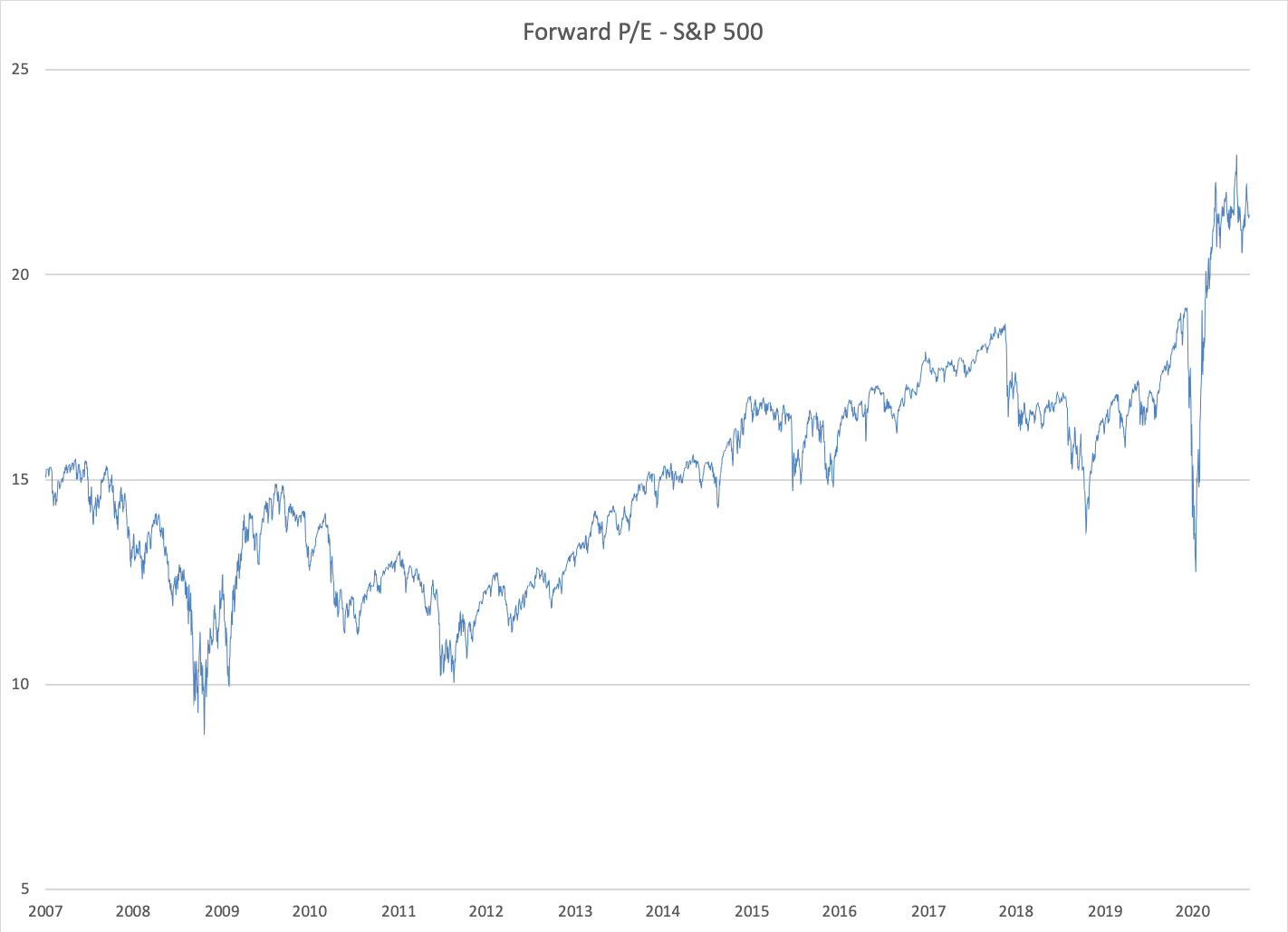

Start with recent evidence for the overall stock market. The major driver of the remarkable recent performance has been the expansion of price-earnings multiples. The graph below plots the S&P 500 one-year forward price-earnings ratio. As shown, it has more than doubled since 2012 despite the fact that it dropped by almost 50% during the onset of the Covid crisis before rising to near record levels. The sharp rise in the P/E ratio makes sense only if the market is looking well beyond current earnings, which have fallen due to the virus, and is instead focusing on the long term.

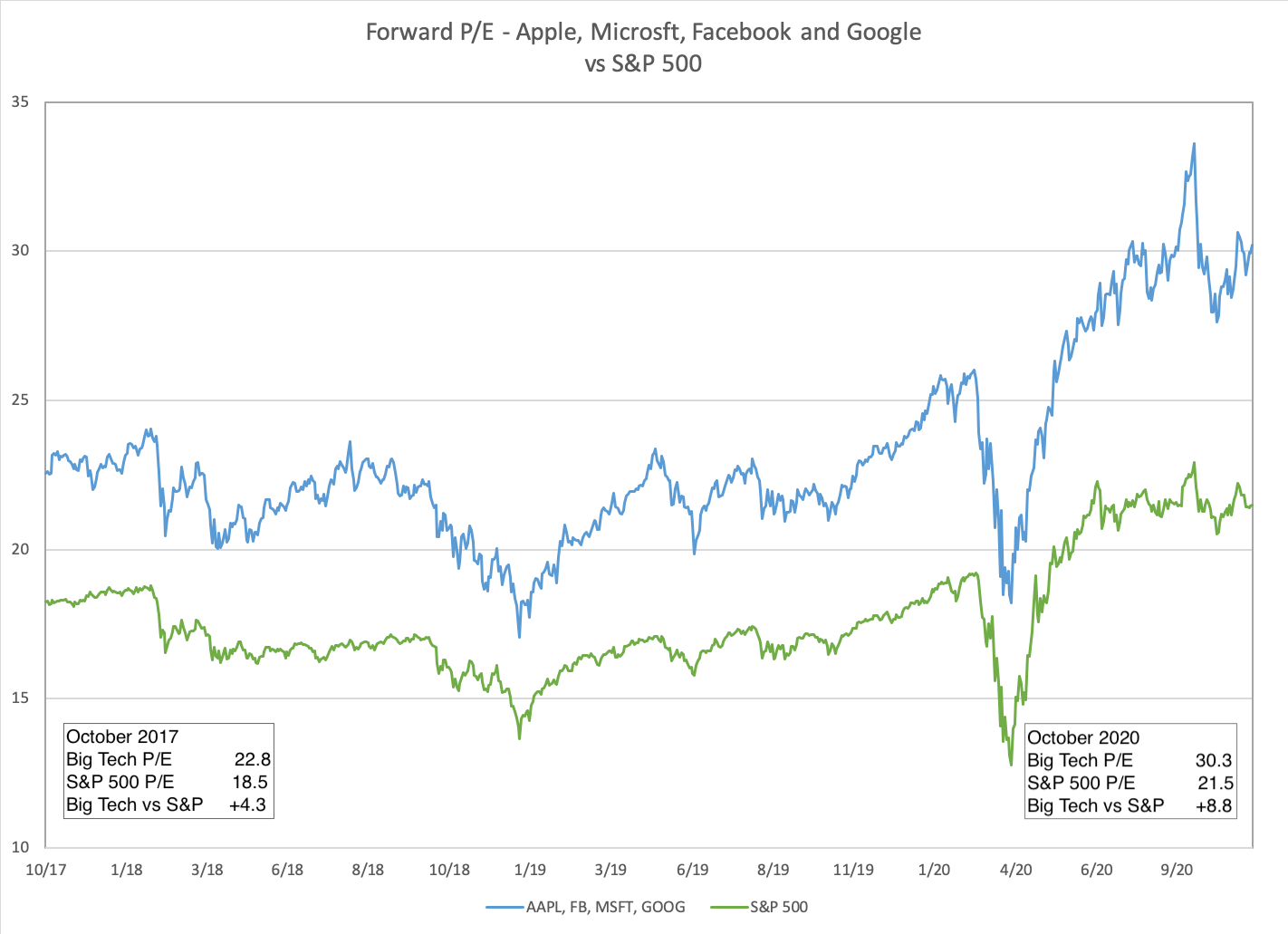

Furthermore, the remarkable market performance has been driven primarily by expansion of the price-earnings multiples for large technology and biotechnology related companies that had high P/Es to begin with. As an example, the graph below plots the average one-year forward price-earnings for Apple, Microsoft, Facebook and Google. Amazon is left off the list because its P/E is so large it would skew the entire plot. The graphs show that the companies that added the most value, did so because of further expansion in their P/E ratios. Once again, the only rational explanation for this behavior is that the market focused on the long term.

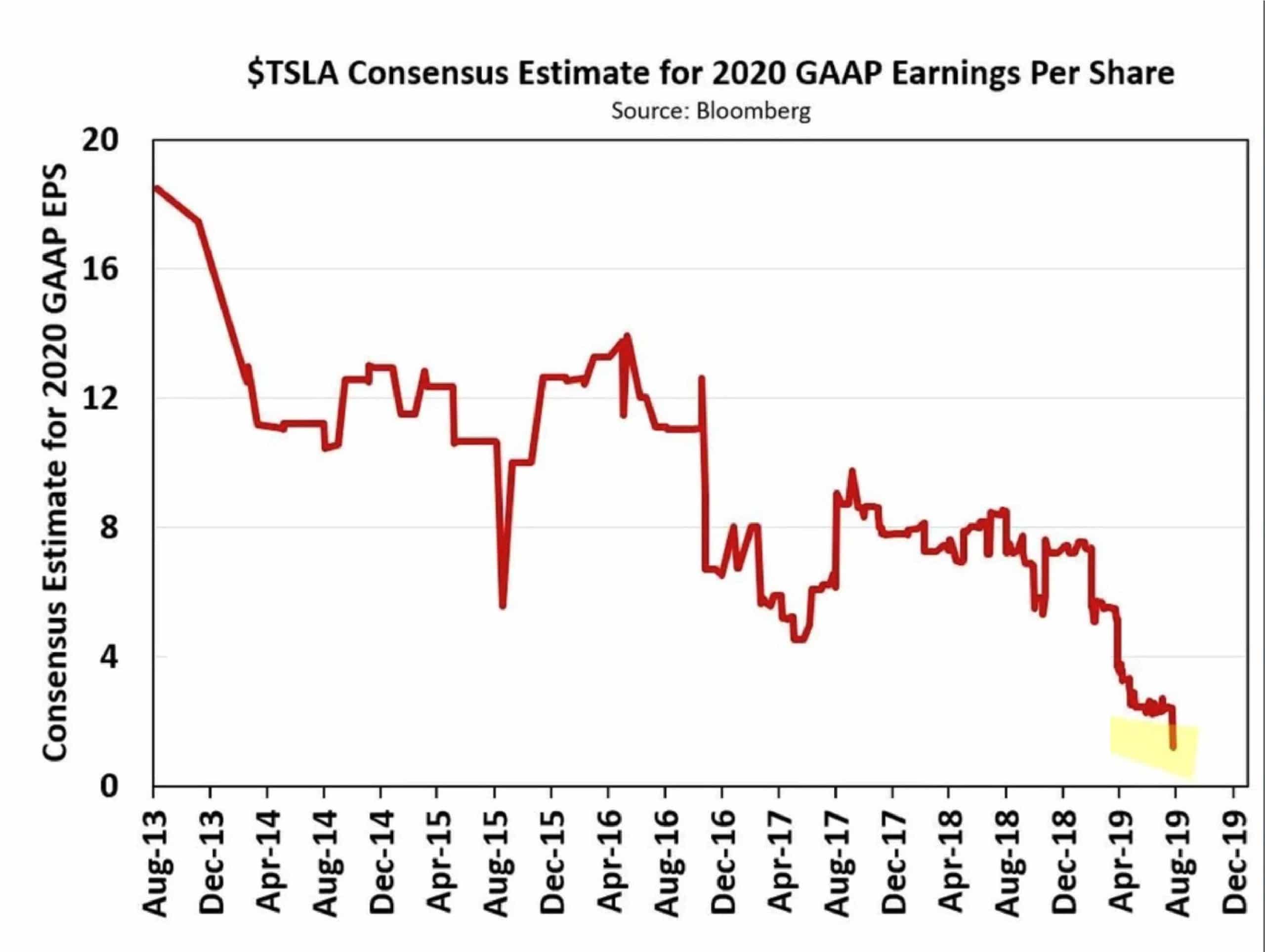

Turning to Tesla, the graph below plots the evolution of consensus estimates for Tesla’s 2020 EPS beginning way back in August of 2013 and running through August 2019. At the start, analysts were forecasting an EPS of $18.00 per share in 2020. With three quarters in the books and only 2 months remaining in the year, the consensus estimate for 2020 EPS is $0.62 per share. You might conclude that Tesla’s market value fell over the years in response to the continuing reduction in estimates for 2020 earnings, but that conclusion is wrong. In fact, the market capitalization of Tesla rose from $60 billion to $400 billion as continuing belief in the long-term success overwhelmed short-term disappointments.

It is worth noting the expansion of the multiples and the associated rise in the market has been asymmetric with companies ratios started with high P/E ratios seeing their ratios rise more than companies that started with low P/E companies. This observation has two implications. First, as a result the value of the overall market has becoming increasingly dominated by high P/E companies. Because of this, investors who buy market index funds now need to be aware that most of their money is being invested in high P/E companies. Second, it means that market values will become increasing sensitive to changes in expected earnings, with this being especially true for high market cap companies with miniscule earnings and huge P/E ratios like Peloton, Tesla, and Zoom. This makes these companies particularly sensitive to new information, a fact that has led to increased volatility and, thereby, attracted day traders. However, it also means that if the companies do not deliver on the long-term expectations driving current prices, precipitous price drops are a distinct possibility.