Interest Rates Inflation And Stock Prices

Given the intense interest in the relation between stock prices, interest rates, and inflation, it is worthwhile to review basic concepts that tie them together. To start, it is critical to be clear w

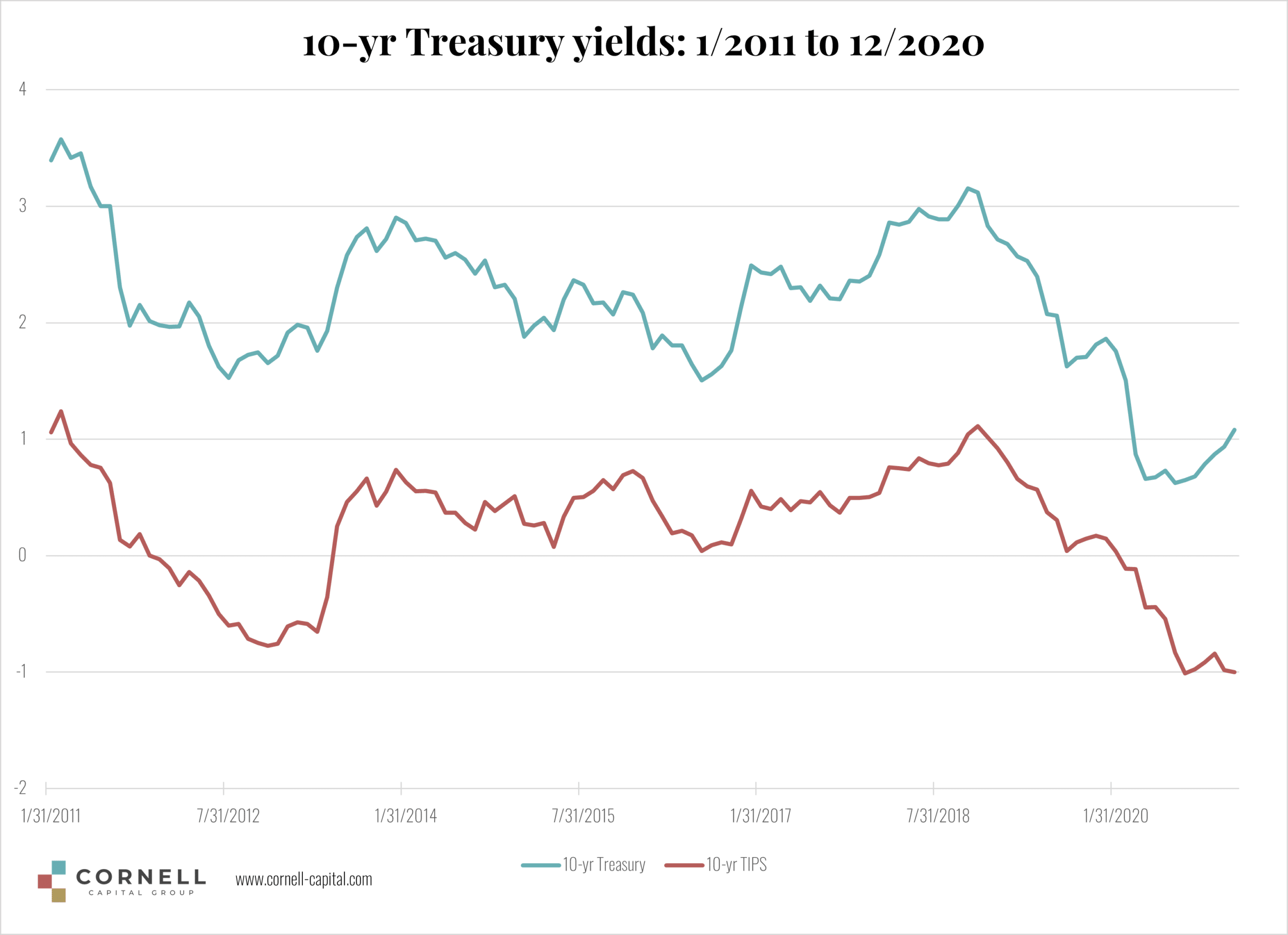

Given the intense interest in the relation between stock prices, interest rates, and inflation, it is worthwhile to review basic concepts that tie them together. To start, it is critical to be clear what is meant by the interest rate – is it real or nominal? To review the difference, the chart below plots the yield on both the constant maturity 10-year Treasury bonds and 10-year Treasury Inflation Indexed Securities or TIPS. If you buy a TIPS you get the stated yield plus an offset for inflation. Therefore, the yield on the TIPS is a real yield because it is what you earn in inflation adjusted dollars, it reflects your increase in purchasing power from the investment.

It takes a moment for the data to sink in. If you buy a 10-year TIPS today, you lose 1% of your purchasing power each year for the next 10 years. By the time the investment matures you will be 10% poorer in real terms (ignoring taxes) than you were at the start. It is hard to imagine a more compelling reason for purchasing stock.

Notice that even though the 10-year nominal yield has recently turned up, the yield on the TIPS has not. That implies greater expected inflation, but not higher real interest rates and it is the real interest rate that theory says should be the main driver of stock prices. This can be seen most easily by applying the constant growth valuation model (although whatfollows istrue in a much more general framework). According to the constant growth model, the value of a company’s stock is given by the relation,

P = FCF / (K – G),

where FCF is next year’s forecast free cash flow, K is the cost of equity capital, and G is the expected growth rate in free cash flow. When you see an equation like this you should immediately ask whether K and G are measured in real or nominal terms. It turns out it doesn’t matter because inflation cancels out! Typically, the cost of equity and the growth rate are measured in nominal terms so each includes the impact of inflation. Therefore, rising interest rates due to higher expected inflation should not depress stock prices, in theory, because they are offset by rising growth in nominal terms. The same is not true of rising real rates which should depress stock prices. When real rates rise, K goes up relative to G without any offset. If K-G rises, stock prices should fall. Therefore, the key interest rate for investors to track is the real rate. And currently, the rate on 10-year TIPS remains at an all-time low.

It is tempting to attribute this state of affairs to Federal Reserve policy, but academic research indicates it if far from clear if the Fed is the explanation. Fed policy can affect short-term nominal rates, but long-term real rates are a different story altogether. This is another reason why investors should stop talking about “ the interest rate.” There are a host of different interest rates with different implications for stock prices. For now, the safest assumption to make is that the record low interest rate on 10-year TIPS remains an unexplained mystery. But whatever the reason for its current level, the future evolution of the 10-year real rate is likely to have a major impact on stock prices. For this reason, it is something that investors should watch closely.