Value Investing Requiem Rebirth Or Reincarnation

For much of the last century, value investors considered themselves to be the winners in the investment world, a result they attributed to their patience, maturity and good sense. That view, at least

BRADFORD CORNELL

ANDERSON GRADUATE SCHOOL OF MANAGEMENT

ASWATH DAMODARAN

STERN SCHOOL OF BUSINESS

Abstract

For much of the last century, value investors considered themselves to be the winners in the investment world, a result they attributed to their patience, maturity and good sense. That view, at least on the surface, was backed up by evidence that “value” stocks, defined as stocks that trade at low multiples of earnings and book value, earned higher returns than “growth” stocks, defined loosely as companies that trade at high multiples of earnings or book value. It was reinforced by the mythology of great value investors, with Warren Buffett and Charlie Munger taking center stage, as deep thinkers, with profound insights on how markets work. In the last two decades, value investing lost its edge, and a debate has revolved around whether this is a temporary phase, and the result of an unusual macro environment, or a reflection of a permanent change in economies and markets. In this paper, we argue that value investing, at least as practiced today, has become rigid and ritualistic, and that while some of its failures can be attributed to external factors, many can be traced back to practices and rules of thumb that have outlived their usefulness. We argue that if value investing is to be successful in the future, it needs to develop a more dynamic view of value and a greater willingness to live with and invest in the face of uncertainty.

The performance of what has conventionally passed for value investing, i.e., buying stocks that trade at low multiples of earnings and book value, in conjunction sometimes with other quantitative and qualitative factors, during the last dozen years has led some analysts and investors to proclaim the demise of this once hallowed strategy and others to argue that this is just a passing phase, with macro forces contributing. In this paper, we examine this question, in the context of history, and evaluate alternative explanations for lagging performance, and possible pathways to a new value investing paradigm.

What is value investing?

Any analysis of value investing has to start with a definition of what it is. Given how widely data services tracking mutual funds classify them into groupings, how quickly prognosticators are able to pass judgment on the successes and failures of value investing, and the vast number of academic papers on value investing, you would think that there is consensus on what comprises value investing, but that is not the case. The definition of value investing varies widely even among value investors, and the differences are often deep and difficult to bridge.

Value Investing and its Many Forms

In this section, we will start by describing three variants of value investing that we have seen used in practice, and then go on to explore a way to find commonalities.

- Mechanical Value Investing: The easiest and most simplistic definition of value investing, and the one that many data services and academics continue to use because it is quantifiable and convenient, and that is to base the distinction between value and growth investing on measures of price to earnings (PE) or price to book (PBV).

- Cerebral Value Investing: More sophisticated value investors, starting with Ben Graham and including Warren Buffett and Charlie Munger, would add that while value investing starts by looking at cheapness (PE and PBV), it also depends on other criteria such as management quality, solid moats, competitive advantages and other qualitative factors.

- Big Data Value Investing: Closely related to cerebral value investing in philosophy, but differing in its roots, is a third and more recent branch of value investing, where investors start with the conventional measures of cheapness (low PE and low PBV) and then look for additional criteria that has separated good investments from bad ones. Those criteria are found by poring over the data and looking at historical returns, a path made possible by access to huge databases and powerful statistical tools. One example of this is defining new valuation ratios that take account of the role of intangible capital.

We take a different twist to defining value investing, arguing that value investors can be broadly classified into four groups, depending on how they approach investment decision making.

Passive Value Investing: Passive value investing amounts to buying and holding stocks based on screens originally described by Benjamin Graham. In The Intelligent Investor,[1] Graham proposed using the following screens:

1. Earnings to price ratio that is double the AAA bond yield.

2. PE of the stock has to be less than 40% of the average PE for all stocks over the last 5 years.

3. Dividend Yield > Two-thirds of the AAA Corporate Bond Yield

4. Price < Two-thirds of Tangible Book Value[2]

5. Price < Two-thirds of Net Current Asset Value (NCAV), where net current asset value is defined as liquid current assets including cash minus current liabilities

6. Debt-Equity Ratio (Book Value) has to be less than one.

7. Current Assets > Twice Current Liabilities

8. Debt < Twice Net Current Assets

9. Historical Growth in EPS (over last 10 years) > 7%

10. No more than two years of declining earnings over the previous ten years.

Any stock that passes all 10 screens, Graham argued, would make a worthwhile investment. In the years since, these screens have been changed, replaced and augmented, but they all still build on the same premise that investing in companies that pass the screens for cheapness, safety and profitability will deliver superior returns.

Contrarian Value Investing: Contrarian value investing is based on the premise that the market overreacts to bad news. The idea is that as the pessimism fades, prices will recover.Activist Value Investing: In activist value investing, the target companies are not only cheap, but also badly run. The payoff to activist value investing comes from activist investors being the catalysts for both price change in the near term, as markets react to their appearance, and to value changes emanating from improvements in how the company is run, in the long term.

Minimalist Value Investing: There is a fourth approach to value investing that perhaps belongs more within passive investing, but for the moment, we will set it apart. In the last decade or two, we have seen the rise of enhanced or tilted index funds and ETFs, where investors start with a market-based index fund or ETF and move away from pure market indexing by overweighting value stocks (low PE/PBV, low volatility etc.) and underweighting non-value stocks. The benefit of this approach is low costs, both in analysis and execution.

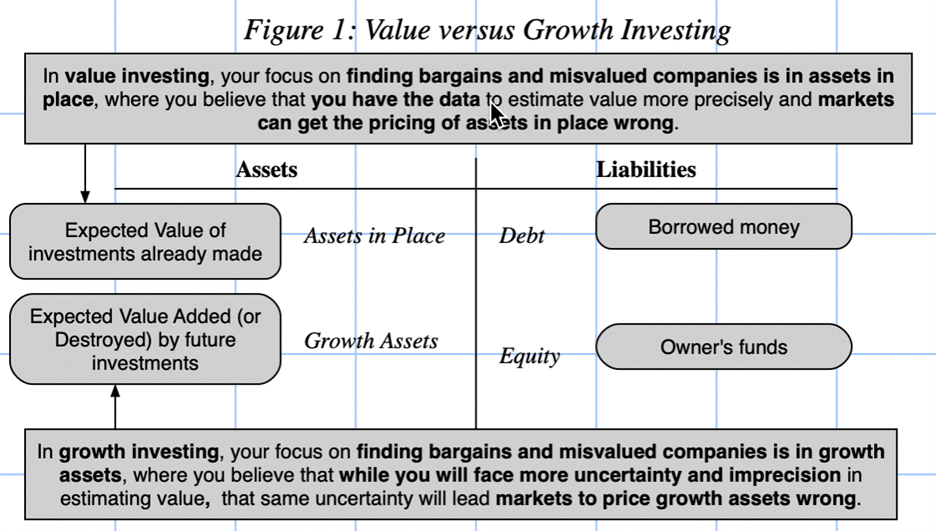

There is a more general approach to framing value investing that encompasses all these approaches and allows you to differentiate value investing from its most direct competitor, growth investing. That approach uses a financial (as opposed to an accounting) balance sheet to draw the contrast and is shown in Figure 1.

In this context, the contrast between value and growth investing is not that value investors care about value and growth investors do not, but in what part of the company the “value error” lies. Value investors believe that their tools and data are better suited to finding mistakes in valuing assets in place, and that belief leads them to focus in on more mature companies, that derive the bulk of their value from existing investments. Growth investors, on the other hand, accept that valuing growth is more difficult and more imprecise, but argue that it is precisely because of these difficulties that growth assets are more likely to be mis-valued.

A short history of value investing

The belief that value investing is a winning philosophy has a deep history. Confidence in value investing is backed by two historical trends; one grounded in stories and practice and the other based on numbers and academic research.

The Story Strand

When stock markets were in their infancy, investors faced two problems. The first was that there were almost no information disclosure requirements, and investors had to work with whatever information they had on companies, or on rumors and stories. The second was that investors, more used to pricing bonds than stocks, drew on bond pricing methods to evaluate stocks, using dividends as replacements for coupons, in evaluating stocks. That is not to suggest that there were not investors who were ahead of the game, and the first stories about value investing come out of the damage of the Great Depression, where a few investors like Bernard Baruch found a way to preserve and even grow their wealth. However, it was Ben Graham, a young associate of Baruch, who laid the foundations for modern value investing, by formalizing his approach to buying stocks and investing in 1934 in Security Analysis , a book that reflected his definition of an investment as “one which thorough analysis, promises safety of principal and adequate return”.[1] In 1938, John Burr Williams wrote The Theory of Investment Value, introducing the notion of present value and discounted cash flow valuation.[2]

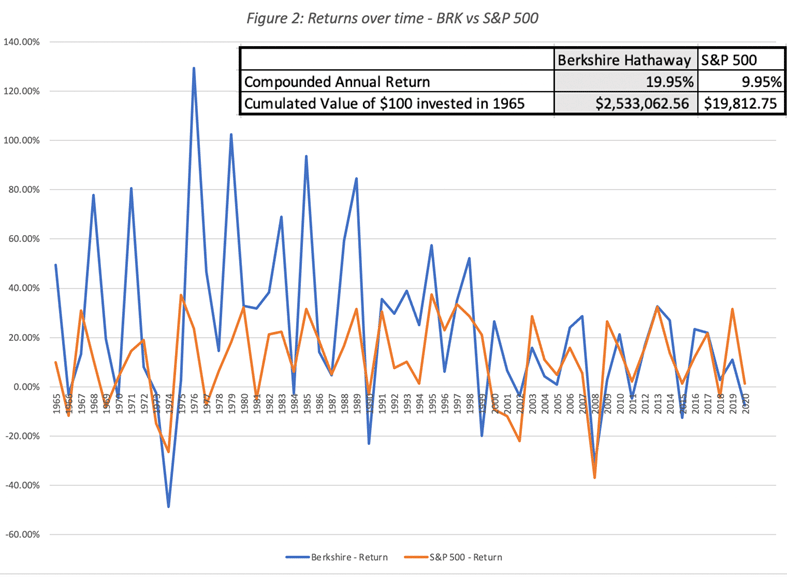

The numbers speak for themselves. Not only did Berkshire Hathaway deliver a compounded annual return that was double that of the S&P 500, it did so with consistency, outperforming the index in 37 out of 55 years. It is true that the returns have looked a lot more ordinary in the last two decades, and we will come back to examine those years in the next section.

Along the way, Buffett proved to be an extraordinary spokesperson for value investing, not only by delivering superior performance, but also because of his capacity to explain value investing with homespun storis and catchy annual letters to shareholders.[1] In 1978, he was joined by Charlie Munger, whose aphorisms about investing have been just as effective at getting investor attention, and were captured well in a book, Poor Charlie’s Almanac.[2] There have been others who have worn the value investing mantle successfully, but it is difficult to overstate how much of value investing as we know it has been built around Graham and Buffett. The Buffett legend has been burnished not just with flourishes like the 1969 partnership letter but by the stories of the companies that he has invested in along the way. Even novice value investors will have heard the story of Buffett’s investment in American Express in 1963, after its stock price collapsed following a disastrous loan to scandalous salad oil company, and quickly doubled his investment.

The Numbers Strand

If all that value investing had going for it were stories about great value investors and their exploits, it would not have the punch that it does today without the help of a numbers strand, ironically delivered by the very academics that many value investors hold in low esteem. To understand this contribution, we need to go back to the 1960s, when finance developed as a discipline, built around beliefs that markets are, for the most part, efficient. The capital asset pricing model was developed in 1964, and for much of the next 15 years, financial researchers tried to test the efficacy of the model. To their disappointment, the model not only revealed clear weaknesses, but it consistently misestimated returns for classes of stock. In 1981, Rolf Banz published a paper, showing that smaller companies (in terms of market capitalization) delivered higher returns, after adjusting for risk with the CAPM, than larger companies.[3] Over the rest of the 1980s, researchers continued to find other company characteristics that seemed to be systematically related to “excess” returns, even though theory suggested that they should not. It is revealing of finance’s early biases that in the early days, these systematic irregularities were called anomalies and not inefficiencies, suggesting that it was not markets that were mispricing these stocks but researchers who were erroneously measuring risk.

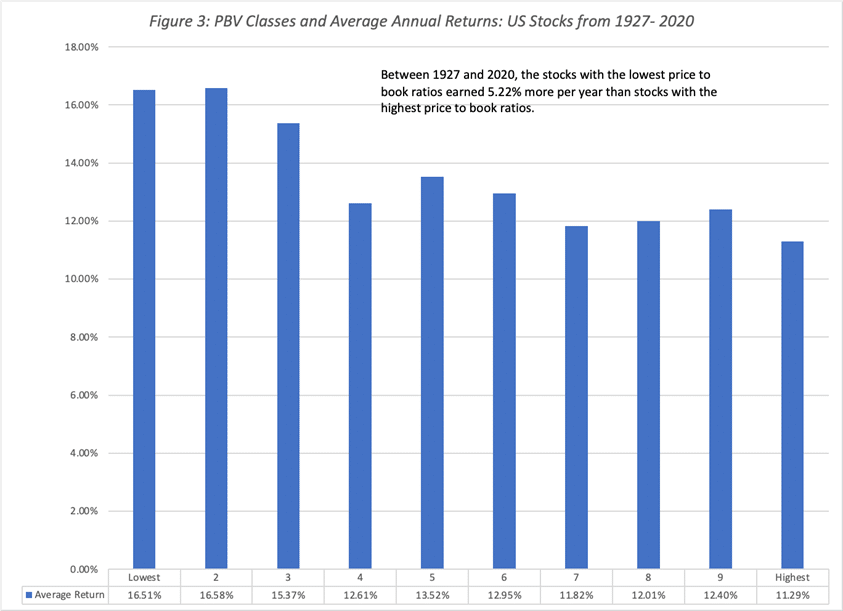

In 1992, Fama and French examined these company characteristics together in a study, where they reversed the research order. Rather than ask whether betas, company size or profitability were affecting returns, they started with the returns on stocks and backed into the characteristics that did best in explaining differences across companies.[4] Their conclusion was that two variables, market capitalization (size) and book to market ratios explained the bulk of the cross-sectional variation in stock returns from 1963 to 1990, and that the other variables were either subsumed by these or played only a marginal role in explaining differences. For value investors, long attuned to book value as a key metric, this research was vindication of decades of investment practice. Figure 3 provides an update on the relation between price to book ratios and returns using data provide by Ken French.

Results similar to Figure 3 have been replicated many times, and in many settings. Dimson, Marsh and Staunton, in their comprehensive annual update on global market returns, note that the value premium (the premium earned by low price to book stocks, relative to the market) has been positive in 16 of the 24 countries that they have returns for more than a century and amounted to an annual excess return of 1.8%, on a global basis.[9]

[While value investors are quick to point to these academic studies as backing for their investment philosophy, they are more reluctant to acknowledge the fact that among researchers, there is a clear disagreement about the reasons for these value premiums:\ \

- It is a proxy for missed risk: In their 1992 paper, Fama and French argued that companies that trade at low price to book ratios are more likely to be distressed and that the CAPM was not doing an adequate job of capturing that risk. While this theory explains the value premium, it does not endorse value investing as a superior strategy. The premium is simply fair compensation for bearing added risk.\

- It is a sign of market inefficiency: During the 1980s, as behavioral finance became more popular, academics became more willing to accept and even welcome the notion that markets make systematic mistakes, largely as a consequence of behavioral quirks and emotional shortcomings. For these researchers, the findings that low price to book stocks were being priced to earn higher returns gave rise to theories of how investor irrationalities could explain these returns. That also opened the door to the possibility that investors less susceptible to these behavioral quirks could take advantage of these mistakes.\ \ It is the latter explanation that reinforces the opinion that value investing is a superior strategy and that the excess returns earned are a reward for this insight.](https://www.cornell-capital.com/blog/2021/02/value-investing-requiem-rebirth-or-reincarnation.html#_ftn1 "")

Value Investing: Story meets Numbers

In the realm of investment philosophies, value investing has had that unique mix work in its favor, with stories of value investors and their winning stocks backed up by numbers on how well value investing has done, relative to other philosophies. It is therefore no surprise that many investors, when asked to describe their investment philosophies, describe themselves as value investors, not just because of its winning track record, but also because of its intellectual and academic backing. When pushed on what their understanding of value investing is, though, these investors come up with divergent reasons, some of which contradict each other. Some genuinely believe in the rostrums of value investing, and their portfolios reflect that belief, filled with mature companies that have “safe” earnings streams and solid cash flows. There are others who talk the value investing talk, but their portfolio choices reflect very different sensibilities. As the old adage goes, to classify investors, you should not look at what they say, but at what they do, and if you follow it, many self-proclaimed value investors are neither focused on value, nor are they investors. Instead, they are traders who play the pricing game, buying and selling on momentum and mood shifts, who adopt the value investing guise, because it gives them gravitas.

The Dark Side of the Good Old Days

For value investors, nostalgic for the good old days, when the dominance of value investing was unquestioned, it is worth pointing out that the good old days were never that good, and that even in those days, there were legitimate questions about the payoff to value investing that remained unanswered or ignored.

Revisiting the Value Premium

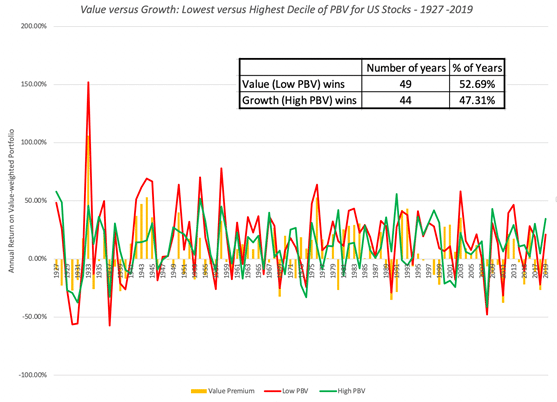

For some value investors, the graph showing that low price to book stocks have outperformed high price to book stocks by more than 5% a year, going back to 1927 in the US, is all the proof they need to conclude that value investing has won the investing game, but even that rosy history has warts that are worth examining. In figure 4, presents year-to-year movements in the value premium, i.e., the difference between the annual returns on the lowest and highest deciles of price to book ratios:

While it is true that low price to book stocks earned higher annual returns than high price to book stocks over the entire time period, there is significant variation over time, High price to book stocks delivered higher returns in 44 of the 93 years. In fact, one of the pitches that growth investors made, with some success, during the glory days of value investing was that you could still succeed as a growth investor if you had the capacity to time the value/growth cycle. Looking back at the year-to-year data on value versus growth and correlating with other variables, there are two fundamentals that seem to be correlated with whether value or growth investing emerges the winner.

- The first is earnings growth, with growth investing beating value investing when earnings growth rates are low, perhaps because growth becomes a scarcer and a bigger driver of value.

- The other is the slope of the yield curve with flatter and downward sloping yield curves associated with growth outperforming and upward sloping yield curves with value outperforming.

In short, the fact that value stocks, at least based upon the price to book proxy, delivered higher returns than growth stocks obscures the reality that there were periods of time even in the twentieth century, where the latter won out. That said, an investor would have to be good at forecasting those periods of low growth and flat yield curves, ahead of their occurrence, to make money on this relationship.

Payoff to Active Value Investing

Investing in low PE or low PBV stocks would not be considered true value investing, by most of its adherents. In fact, most value investors argue that the while value investing may start with these stocks, the real payoff to value investing comes from the additional analysis, whether it be in bringing in other quantitative screens (following Ben Graham) and qualitative ones (good management, moats). If we call this active value investing, the true test of value investing then becomes whether following value investing precepts and practices and picking stocks generates returns that exceed the returns on a value index fund, created by investing in low price to book or low PE stocks. Defined thus, the evidence that active value investing works has always been weak, though it varies depending upon the strand of value investing examined.

- Screening for Value: Since Ben Graham provided the architecture for screening for cheap stocks, it should be no surprise that some of the early research looked at whether Graham’s screens worked in delivering superior returns. Henry Oppenheimer examined the returns on stocks, picked using the Graham screens, between 1974 and 1981, and found that they delivered average excess returns of about 17% a year.[10] There are other studies that come to the same conclusion, looking at screening over the same period, but they all suffer from two fundamental problems. The first is that one of the value screens that invariably gets used is low PE and low PBV, and we already know that these stocks delivered significantly higher returns than the rest of the market for much of the last century, and it is unclear from these studies whether all of the additional screens (Graham has a dozen or more) add much to returns. The second is that the ultimate test of a philosophy is not in whether its strategies work on paper, but in whether the investors who use those strategies make money on actual portfolios. There is many a slip between the cup and the lip, when it comes to converting paper strategies to practical ones and finding investors who have consistently succeeded at beating the market, using screening, is difficult to do.

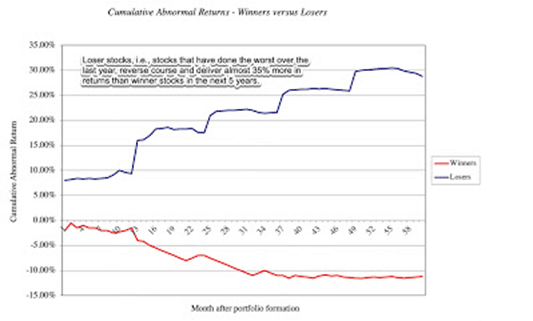

- Contrarian Value: The early evidence on contrarian investing came from looking at loser stocks, i.e., stocks that have gone down the most over a prior period and chronicling the returns from buying these stocks. One of the earliest studies, from the mid 1980s, presented the eye-catching graph shown in Figure 5, backing up the thesis that loser stocks are investment winners:[11]

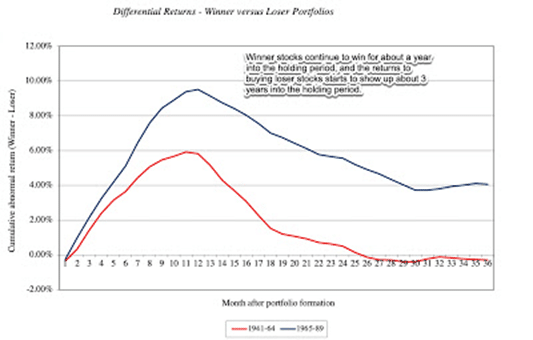

In this study, loser stocks, defined as the stocks that have gone down the most in the last year, deliver almost 45% more in returns than winner stocks, defined as stocks that have gone up the most in the last year. Before you jump out and start buying loser stocks, research in subsequent years pointed to two flaws. The first was that many of the loser stocks in the study traded at less than a dollar, and once transactions costs were factored in, the payoff to buying these stocks shrunk significantly. The second came in a different study, which made a case for buying winner stocks with the graph in Figure 6:[12]

Note that in Figure 6 winner stocks continue to win, in both time periods examined, in the first twelve months following portfolio formation, though those excess returns fade in the months thereafter. Put simply, if you invest in loser stocks and lose your nerve or your faith, and sell too soon, the loser stock strategy will not pay off.

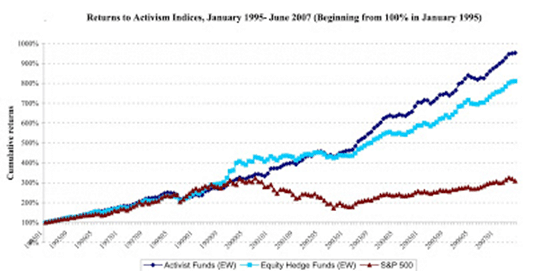

- Activist Value: Of all of the different strands of value investing, the one that seems to offer the most promise is activist investing, because it is a club that only those with substantial resources can join, with the promise of bringing change to companies. The early results looked promising, as activist hedge funds appeared to beat the market as shown in Figure 7:[13]

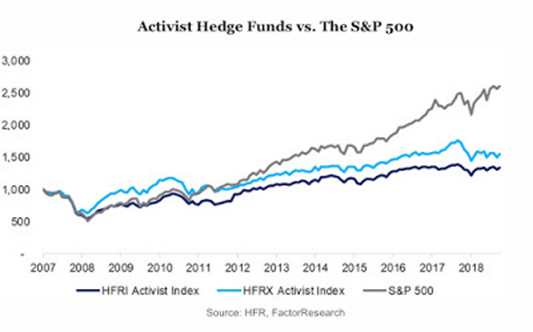

In the 1995-2007 time-period, activist value investors outstripped both hedge funds and the S&P 500, delivering significantly higher returns. Those numbers, though, started to come under strain, as activist investing widened its search and perhaps lost its focus in the last decade, as can be seen in Figure 8.[14] However, in the last decade, the bloom has come off the activist investing rose, and activist investors, at least in the aggregate, underperformed the market.

- Indexed Value: Many value investors will blanch at the idea of letting indexed value investors into this group, but there can be no denying the fact that funds have flowed into tilted or enhanced index funds, with many of the tilts reflecting historical value factors (low price to book, small cap, low volatility). The sales pitch for these funds is more often that you can not only get a higher return, because of your factor tilts, but also a bigger bang (return) for your risk (standard deviation) rather than a higher return per se (higher ratios of returns to standard deviation). The jury is still out, and our personal view is titled index funds are an oxymoron, and that these funds should be categorized as minimalist value funds, where investors try to minimize activity, so as to lower costs.

The most telling statistics on the failure of value investing come from looking at the performance of mutual fund managers who claim to be its adherents. While the earliest studies of mutual funds looked at them as a group, and concluded that they collectively under-performed the market, later studies have looked at mutual funds, grouped by category (small cap vs large cap, value vs growth) to see if fund managers in any of these groupings performed better than managers in other groupings. Very few of these studies have found any evidence that value fund managers are more likely to beat their index counterparts than their growth fund counterparts. It is telling that value investors, when asked to defend their capacity to add value to investing, almost never reference that research, partly because there is little that they can point to as supportive evidence, but instead fall back on Warren Buffett, as their justification for value investing.

Wandering in the wilderness? Value Investing in the last decade

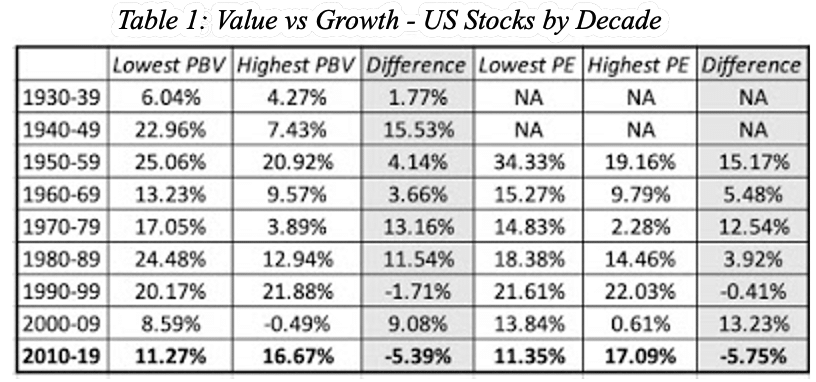

The last decade has, in our view, tested value investing in ways not seen heretofore. To see how much of an outlier this period (2010-2019) has been, take a look at the returns to low and high PBV stocks, by decade, from 1930 to 2019, presented in Table 1.

While it is true that the dot-com boom allowed growth stocks to outperform value stocks in the 1990s, the difference was small and concentrated in the last few years of that decade. In the 2010-2019 time period, in the battle between value and growth, it was no contest with growth winning by a substantial amount and in seven of the ten years.

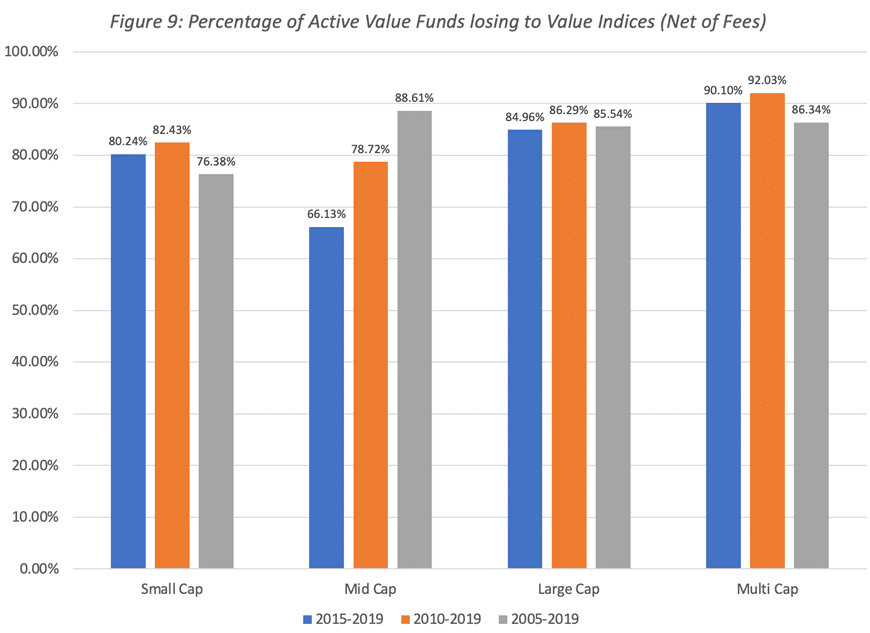

To make things worse, active value investors, or at least those that run mutual funds, found ways to underperform even the badly performing value indices. One of S&P’s most informative measures is SPIVA, where S&P compares the returns of fund managers in different groupings to indices that reflect that grouping (value index for value funds, growth index for growth funds etc.) and reports on the percentage of managers in each grouping that beat the index. In Figure 9, we report the SPIVA measures for 2005-2019 for value managers in all different market cap classes (large, mid-sized, small):

Put simply, the great majority of value fund managers failed to beat the value indices, net of fees. Even gross of fees, the percentages of fund managers beating their indices was well below 50%.

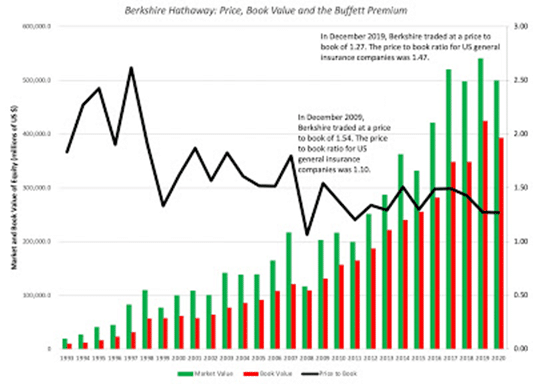

Legendary value investors lost their mojo during the decade, and even Warren Buffett’s stock picking delivered average returns. He abandoned long standing practices, such as using book value as a basis for estimating intrinsic value and never doing buybacks, for good and bad reasons. One indicator the measures how the market has adjusted its assessment of Mr. Buffett’s stock picking skill is a number that has the Buffett imprimatur, the ratio of price to book at Berkshire plotted in Figure 10. The premium that investors are paying over Berkshire’s book value can be interpreted to be a stock picker premium.

Because the importance of Berkshire’s insurance business, we compared the price to book for Berkshire to that of general insurance companies listed and traded in the United States. At the start of 2010, Berkshire traded at a price to book ratio of 1.54, well above the US insurance company industry average of 1.10. Ten years later, at the start of 2020, the price to book ratio for Berkshire had dropped to 1.27, below the average of 1.47 for US insurance companies. The loss of the Buffett premium may seem puzzling to those given his reputation an investing deity. Our reading is that markets are less sentimental and more realistic in assessing both the quality of his investments and the fact that at his age, Mr. Buffett may be passing the baton to younger investment managers.[15]

The COVID shock

For much of the last decade, value investors argued that their underperformance was a passing phase, driven by the success of growth and momentum and aided and abetted by the Fed, and that value investing would come back with a vengeance in a crisis. The viral shock delivered by the Corona Virus early tin 2020 seemed to offer an opportunity for value investing, with its emphasis on safety and earnings, to shine. In the first few weeks, there were some in the value investing camp who argued that following old time value investing precepts and investing in stocks with low PE and Price to book ratios and high dividends would help buffer investors from downside risk.

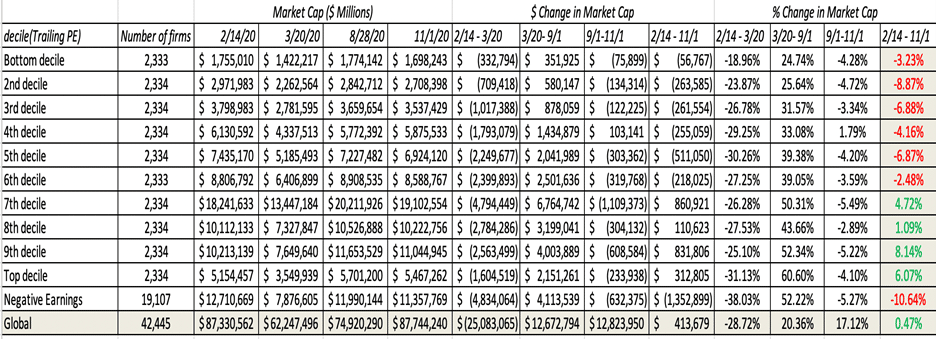

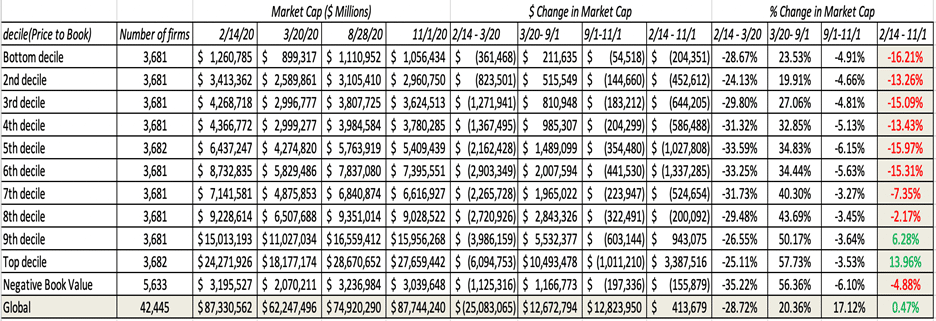

While the logic may have been appealing, the results have not been as hoped. In Table 2 we sort stocks into deciles on the basis of their PE ratios and Price to Book ratios as of February 14, 2020 (at the start of the crisis), and report the changes in the aggregate market capitalization in the nine months following:

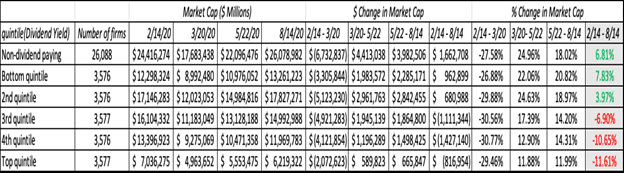

The numbers speak for themselves. Low PE and low PBV stocks lost value during this crisis, whereas high PE and PBV stocks gained in value. Breaking companies down in quintiles based upon dividend yields, yields a similar results as shown in Table 3. The higher the dividend yield, that is the more value oriented the stock, the worse the performance. Overall, the results are perverse, at least from a value investing perspective, the stocks that have done best in this crisis are non-dividend paying, high PE stocks, and the stocks that have done worst during the crisis have been high dividend paying, low PE companies.

The Explanations

The attempt to explain what happened to value investing in the last decade (and during COVID) is not just about explaining the past, because the explanation may affect assessments of value investing going forward. There are five explanations that we have heard from value investors for what were wrong during the last decade, and we will list them in their order of consequence for value investing practices, from most benign to most consequential.

- 1. This is a passing phase!

- Diagnosis: Even in its glory days, during the last century, there were extended periods (like the 1990s) when low PE and low PBV stocks underperformed, relative to high PE and high PBV stocks. The last decade was one of those aberrations, and as with previous aberrations, it too shall pass!

- Prescription: Be patient. With time, value investing will deliver superior returns.

- Assessment: If this is a passing phase, it is a very long one.

- 2. The Fed did it!

- Diagnosis: Starting with the 2008 crisis and stretching into the last decade, central banks around the world have become much more active players in markets. With quantitative easing, the Fed and other central banks have contributed not only to lower interest rates but also provided protection for risk taking at the expense of conservative investing (often called the Greenspan put).

- Prescription: Central banks cannot keep interest rates low in perpetuity, and they do not have the resources to bail out risk takers forever. Eventually, the process will blow up, causing currencies to lose value, government budgets to implode, and inflation and interest rates to rise. When that happens, value investors will find themselves less hurt than other investors.

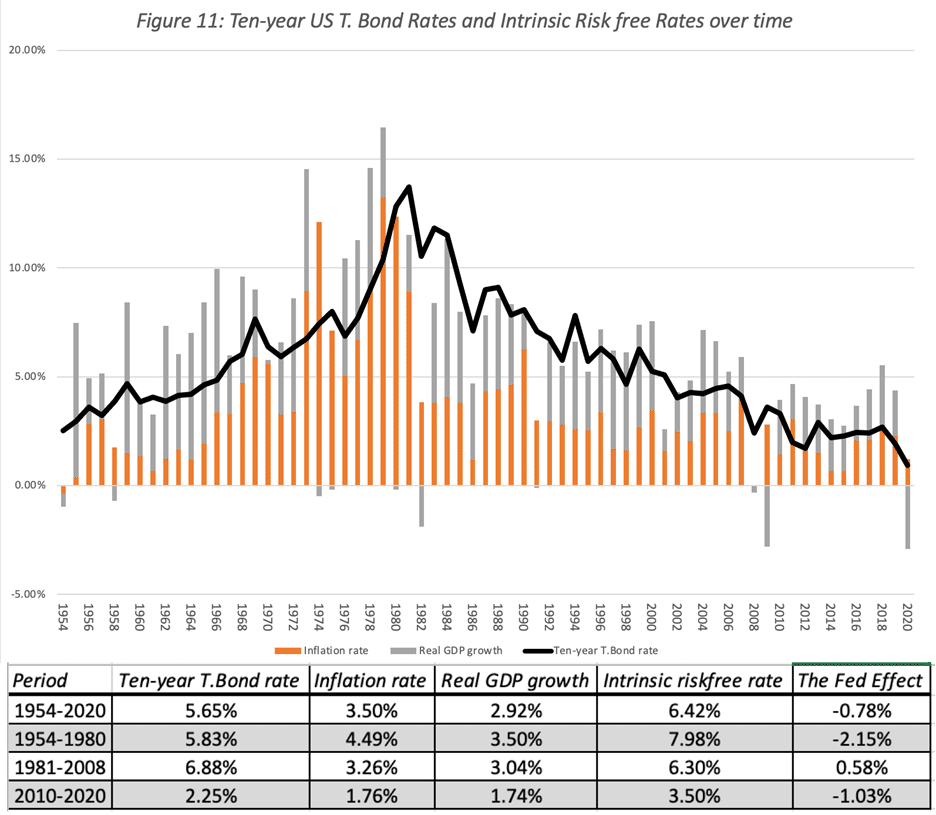

- Assessment: To buy into this story, you also have to believe that the main reason for low interest rates is central bank intervention. This belief, though widely held, is at war with both the limited powers that central banks have to set rates as well as fundamentals. In fact, rates have been low primarily because inflation has stayed low and economic growth has been anemic for the last decade, as illustrated by Figure 11.

- Has the Fed had an effect on interest rates in the last decade? Of course, but that effect is actually smaller than what we saw between 1954 and 1980, and the overwhelming reason for low rates was a combination of low inflation and low real growth.

- 3. It’s the accountants’ fault

- Diagnosis: Accounting, as we know it, was designed to measure earnings and asset value at manufacturing firms and it has struggled, as a discipline, with firms that don’t fit that mold. For instance, accounting has miscategorized R&D and operating leases as operating expenses, when the former is a capital expenditure and the latter a financial expense. As a consequence, balance sheets at firms with substantial R&D and operating lease expenses will fail to reflect assets that are created by these expenses and the book value will be understated. Value investing approaches built around book value will therefore find technology, pharmaceutical and service companies to be overpriced, even when they are not.

- Prescription: If you could rewrite accounting rules to reclassify expenses consistently, balance sheets will incorporate missing assets and perhaps allow them to pass price to book value tests. In good news for value investors, accounting is already moving in this direction, with both IFRS and GAAP requiring that all leases be treated as debt, starting in 2019, and the push towards bringing intangibles on to the books.[16]

- [Assessment: Fixing the inconsistencies in accounting will make book values of companies in some sectors (service, technology, pharmaceuticals) more realistic, but it will still do little to compensate for the fact that accounting is not designed to, nor should it even try to, estimate the value of future growth. Value investors should be able to start with the basic accounting data and reclassify items as needed.\

\

- 4. The Investment World has become flatter!\ \

- Diagnosis: When Ben Graham listed his screens for finding good investments in 1949, running those screens required data and tools that most investors did not have access to, or the endurance to run. All of the data came from poring over annual reports, often using very different accounting standards, the ratios had to be computed with slide rules or on paper, and the sorting of companies was done by hand. Even into the 1980s, access to data and powerful analytical tools was restricted to professional money managers and thus remained a competitive advantage. As data has become easier to get, accounting more standardized, and analytical tools more accessible, there is very little competitive advantage to computing ratios (PE, PBV, debt ratio etc.) from financial statements and running screens to find cheap stocks. However, this explains only why value stocks should no longer outperform, it does not explain a significant decade of underperformance.\ \

- Prescription: To find a competitive edge, value investors have to become creative in finding new screens that are either qualitative or go beyond the financial statements or in finding new ways of processing publicly accessible data to find undervalued stocks.\ \

- Assessment: We believe that the leveling of investment resources will continue and achieving superior performance will require greater creativity and judgement going forward.\ \

- 5. The global economy has changed!\ \

- Diagnosis: At the risk of sounding cliched, the shift in economic power to more globalized companies, built on technology and immense user platforms, has made many old-time value investing nostrums useless.\ \

- Prescription: Value investing has to adapt to the new economy, with less balance sheet focus and more flexibility. Value investors may have to leave their preferred habitat (mature companies with physical assets bases) in the corporate life cycle to find value.\ \

- Assessment: As disruption and change come to almost every sector, investing techniques built around mean reversion may well deliver perverse results.](https://www.cornell-capital.com/blog/2021/02/value-investing-requiem-rebirth-or-reincarnation.html#_ftn1 "")

Value Investing: Has it lost its way?

We have never made the pilgrimage to the Berkshire Hathaway meetings, but we do think that value investing had lost its way at three levels.

- It has become rigid: In the decades since Ben Graham published Security Analysis, value investing has developed rules for investing that have no give to them. Some of these rules reflect value investing history (screens for current and quick ratios), some are a throwback in time, and some just seem curmudgeonly. For instance, value investing has been steadfast in its view that companies that do not have significant tangible assets, relative to their market value are not investment candidates. That view has kept many value investors out of technology stocks for most of the last three decades. Similarly, value investing’s focus on dividends has caused adherents to concentrate their holdings in utilities, financial service companies and older consumer product companies, as younger companies have shifted toward returning cash in buybacks.

- It has become ritualistic: The rituals of value investing are well established, from the annual trek to Omaha, to the claim that your investment education is incomplete unless you have read Ben Graham’s Intelligent Investor and Security Analysis to an almost unquestioning belief that anything said by Warren Buffett or Charlie Munger has to be right.

- It has become righteous: While investors of all stripes believe that their “investing ways” will yield payoffs, some value investors seem to feel entitled to high returns because they have followed all of the rules and rituals. In fact, they view investors who deviate from the script as shallow speculators, who will fail in the “long term”.

Put simply, value investing, at least as practiced by some of its advocates, has evolved into a religion, rather than an investment philosophy.

A New Paradigm for Value Investing

For value investing to rediscover its roots and reclaim its effectiveness, we believe that it has to change in fundamental ways.

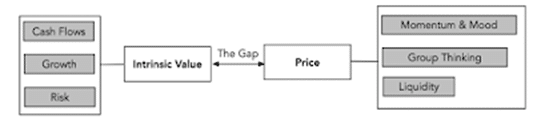

- Be clearer about the distinction between value and price: While value and price are often used interchangeably by some market commentators, they are the results of very different processes and require different tools to assess and forecast. In Figure 12, we contrast the price and value process.

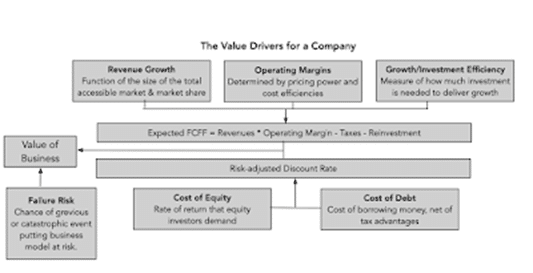

Value is a function of cash flows, growth and risk, and any intrinsic valuation model that does not explicitly forecast cash flows or adjust for risk is lacking core elements. Price is determined by demand and supply and influenced by mood and momentum. One way to, price an asset is by looking at how the market is pricing comparable assets. We are surprised that so many value investors seem to view discounted cash flow valuation as a speculative exercise, and instead base their analysis on a comparison of pricing multiples (PE, Price to book etc.). After all, there should be no disagreement that the value of a business comes from its expected future cash flows, and the uncertainty associated with those cash flows as illustrated in Figure 13.

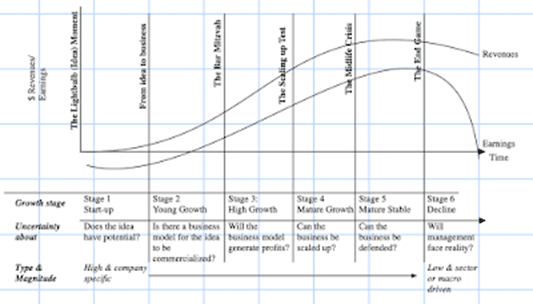

2. Dont avoid uncertainty; face up to it: Many value investors view uncertainty as “bad” and “something to be avoided.” It is this perspective that has led them away from investing in growth companies, where you have to grapple with forecasting the future and towards investing in mature companies with tangible assets. The truth is that uncertainty is a feature of investing, not a bug, and that it always exists, even with the most mature, established companies, albeit perhaps in smaller doses. One way to illustrate the evolution of uncertainty is with reference to the corporate life cycle as depicted in Figure 14.

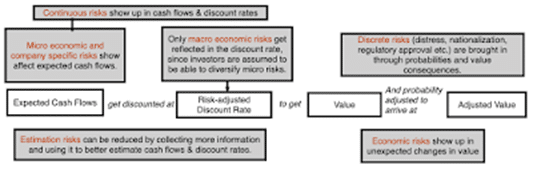

While it is true that there is less uncertainty, when valuing more mature companies in stable markets, you are more likely to find those mistakes in companies where the uncertainty is greatest about the future, either because they are young or distressed, or because the macroeconomic environment is challenging. In fact, uncertainty underlies almost every part of intrinsic value, whether it be from micro to macro sources, as depicted in Figure 15.

To deal with that uncertainty, value investors need to expand their toolboxes to decision trees and Monte Carlo simulations.

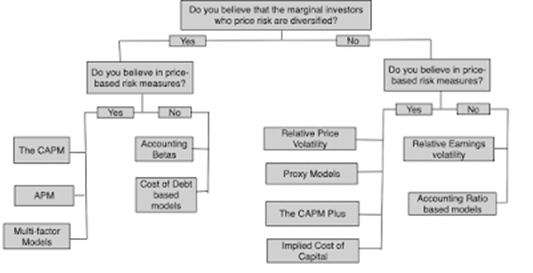

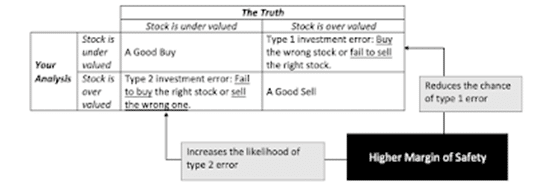

3. Margin of safety is not a substitute risk measure: Although many value investors reject the tools of modern portfolio theory, but careful risk analysis is still required. Fundamental valuation is flexible enough to allow to allow investors to use risk measures other than standard betas as shown in Figure 16.

For those value investors who argue that the margin of safety is a better proxy for risk, it is worth emphasizing that the margin of safety comes into play only after you have valued a company, and to value a company, you need a measure of risk. When used, the margin of safety creates tradeoffs, where you avoid one type of investment mistake for another, as illustrated in Figure 17.

Whether having a large margin of safety is a net plus or minus depends in large part on the success of fundamental valuation. A margin of safety that is too large may lead the investor to hoard cash and forego potentially profitable investments.

1. Don’t expect accounting changes to rescue value investing: It is undeniable that value investing has an accounting focus, with earnings and book value playing a central role in investing strategies. There is good reason to trust those numbers less now than in decades past, for a few reasons. One is that companies have become much more aggressive in playing accounting games, using pro forma income statements to skew the numbers in their favor. The second is that as the center of gravity in the economy has shifted away from manufacturing companies to technology and service companies, accounting has struggled to keep up. While some value investors and accountants seem to believe that once the accounting inconsistencies are eliminated, book value and value investing are poised for a comeback, we disagree. Even if accounting managed to find a way to bring consistency to expensing and capitalization across businesses, all it can accomplish is delivering a better estimate of the value of assets in place. In fact, the value of future growth is not an accounting issue, but an estimation one, and the failure of value investing is not that the accounting mechanics do not work but lie deeper.

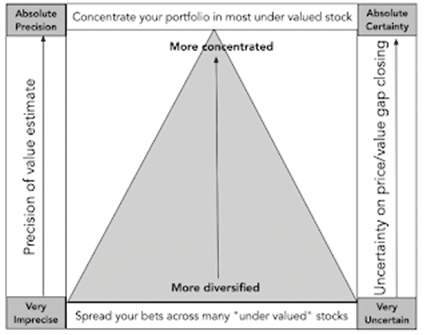

2. You can pick stocks, and be diversified, at the same time: While not all value investors make this contention, a surprisingly large number seem to view concentrated portfolios as a hallmark of good value investing, arguing that spreading your bets across too many stocks will dilute your upside. The choice of whether you want to pick good stocks or be diversified is a false one, since there is no reason you cannot do both. Our reasoning for diversification is built on the presumption that any investment, no matter how well researched and backed up, comes with uncertainty regarding the payoff. In figure 17, we present the choice between concentration and diversification in terms of precision of the investor valuation and uncertainty about the market closing the valuation gap.

We believe that value investors are on shaky ground assuming that doing your homework and focusing on mature companies will yield precise valuations, and on even shakier ground, when assuming that markets correct valuation mistakes in a timely fashion. In a market, where even the most mature of companies are finding their businesses disrupted and market momentum is augmented by passive trading, having a concentrated portfolio is foolhardy.

6. Don’t feel entitled to be rewarded for your virtue: Investing is not a morality play, and there are no virtuous ways of making money. The distinction between investing and speculating is not only a fine one, but very much in the eyes of the beholder. The only reason for concluding that value investing is superior to any strategy is evidence that it produces superior risk adjusted returns. In light of the behavior of stock prices in the last decade that evidence is at best mixed.

Conclusion

Investors, when asked to pick an investment philosophy, gravitate towards value investing, drawn by the work of Benjamin Graham, the reputation of Warren Buffett, and the history of success in markets. While that dominance was unquestioned for much of the twentieth century, when low PE/PBV stocks earned significantly higher returns than high PE/PBV stocks, the last decade has shaken the faith of even diehard value investors. While some value investors see this as a passing phase or the result of central banking overreach, we believe that value investing has lost its edge, partly because of its dependence on measures and metrics that have become less meaningful over time and partly because the global economy has changed, with ripple effects on markets. To rediscover itself, value investing needs to get over its discomfort with uncertainty and be more willing to define value broadly, to include not just countable and physical assets in place but also investments in intangible and growth assets.

[1] Graham, B., 1949, The Intelligent Investor, Harper & Brothers, New York.

[2] Tangible Book value is computed by subtracting the value of intangible assets such as goodwill from the total book value.

[3] Graham, B. and D. Dodd, 1934, Security Analysis, McGraw-Hill.

[4] Williams, J.B., 1938, The Theory of Investment Value, Fraser Publishing.

[5] The archived shareholder letters, going back to 1977, are available at this link: https://www.berkshirehathaway.com/letters/letters.html

[6] Munger, C.T., 2005, Poor Charlie’s Almanack, The Donning Company.

[7] Banz, R., 1981, The Relationship betwween Return and Market Value of Common Stocks, Journal of Financial Economics, v9, 3-18.

[8] Fama, E.F. and K.R. French, 1992, The Cross-Section of Expected Returns, Journal of Finance, v47, 427-466.

[9] Dimson, E., P Marsh and M Staunton, Credit Suisse Global Investment Returns Yearbook, 2020, Credit Suisse/ London Business School.

[10] Oppenheimer, H.R., 1984, A Test of Ben Graham’s Stock Selection Criteria, Financial Analysts Journal, v40, 68-74.

[11] DeBondt , W.F.M. & R. Thaler, 1987, Further Evidence on Investor Overreaction and Stock Market Seasonality, Journal of Finance, v42, pp 557-581.

[12] Jegadeesh, N. and S. Titman, 1993, Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency, Journal-of-Finance; 48(1), 65-91.

[13]Brav, A., 2008, The Returns to Hedge Fund Activism, ECGI Working Paper.

[14]Rabener, N., 2019, Do activist investors create value? CFA Institute.

[15] To illustrate, Berkshire Hathaway attracted widespread meida attention when the company announced that they intended to invest in Snowflake, a small, money-losing tech company in the cloud space, in 2020. If this is a “value” investment, then it seems like Berkshire has redefined the value strategy. Perhaps the younger generation of investors, who have a different defintion of value investing from that traditonally employed by Mr. Buffet, were responsible for the decision.

[16]Lev, B., 2018, Intangibles, SSRN Working Paper (https://papers.ssrn.com/sol3/papers.cfm?abstract\_id=3218586).