Valuing The Automotive Industry

By Bradford Cornell, Shaun Cornell, Andrew Cornell

By Bradford Cornell, Shaun Cornell, Andrew Cornell

Introduction

An investor would have to have been living under a rock not to have noticed the appreciation in the value of automobile companies in the last two years. Tesla, of course, is the premier example. In less than two years, its market capitalization has soared from less than $100 billion to over $1.2 trillion at one point. But Tesla is hardly alone. Recent electric entrants like Xpeng, Nio, Rivian, and Lucid have all seen their valuations jump. Even traditional automakers like Ford, GM and Volkswagen saw their valuations rise when they announced electric vehicle plans.

This across-the-board run-up is sufficiently unprecedented that it calls for a valuation analysis of the automotive industry. Are the price increases consistent with reasonable fundamental valuation – for all companies in the industry or just a small group? What are the investment implications?

Before turning to the data and analysis, there is a key economic principle related to technological innovation and valuation that must be kept in mind. Specifically, a new technology does not translate into value creation for a company that adopts it unless it produces returns on invested capital (ROIC) in excess of the cost of capital. To earn excess returns, there must be barriers to entry that prevent competitors from adopting the technology, entering the business and driving down the ROIC to the cost of capital.

“Although the invention of the aircraft was a great leap forward that created a vast amount of social value, that value was captured almost exclusively by customers, not airlines”

Without significant barriers to entry, none of the firms in the industry can create significant value, so that the enterprise value (EV) will be only slightly greater than the capital supplied by investors, commonly referred to as invested capital (IC). Warren Buffett offers the air travel business an example. Although the invention of the aircraft was a great leap forward that created a vast amount of social value, that value was captured almost exclusively by customers, not airlines. Due to competition over the course of the last century, virtually every company in the airline industry either failed or merged into a larger airline, most of which also collapsed. Those that have survived have EV/IC ratios approximately equal to 1.0.

The history of the automotive industry has been similar. Wikipedia provides a comprehensive list of approximately 500 defunct American automobile manufacturers. The companies on the list disappeared for various reasons, such as bankruptcy of the parent company, mergers, or being phased out. The list also includes companies like General Motors that went bankrupt but were able to emerge and survive, in part with the help of government assistance. To say that historically the industry has been competitive and capital intensive is an understatement. The question is whether the future will be more of the same or whether the inevitable move to electric powered cars will somehow change industry dynamics and the valuation of constituent companies.

Valuation Analysis

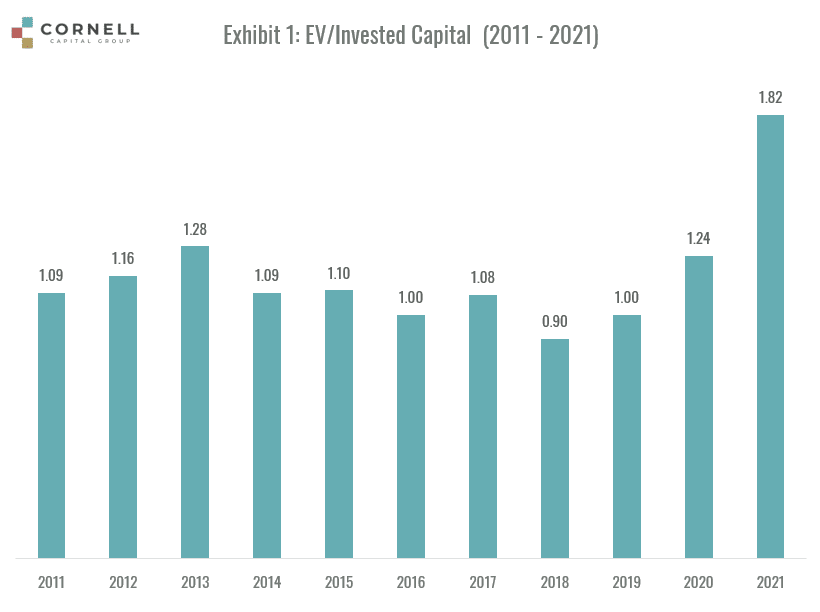

Based on the foregoing, our analysis of the automotive industry starts with data on the EV/IC ratio. Exhibit 1 presents data on the EV/IC ratio compiled by Prof. Aswath Damodaran over the years from 2011 to 2021. We note that Prof. Damodaran includes all of the company’s debt, including that issued by financing subsidiaries, in his measure of invested capital.

The exhibit shows that prior to 2020 the ratio bounced around its average of 1.08 with no observable trend indicating that the industry was only creating a modicum of investor value. (To provide perspective, the ratio for the software industry was 9.37 in 2020.) In 2020, however, the ratio rises to 1.24 and then it jumps all the way to 1.82 by November 1, 2021, well above its historical high-water mark.

The primary reason for the increase in the EV/IC ratios is the rising importance of electric vehicle specialists and their extraordinary ratios. For example, in November 2021, Tesla had an EV/IC ratio of 52.7, a level in excess of that achieved by Amazon and Apple. The sky-high ratio is a result of three factors. First, and most basically, it is a result of investor enthusiasm for the stock. Second, the IC is reduced by the fact that Tesla does not have a financing subsidiary. Third, Tesla, like many of the other new EV companies, holds are large amount of cash. That cash is deducted in the calculation of invested capital despite the fact that much of it is being held to pay for new investments and can, therefore, be thought of as part of invested capital. The combination of the nosebleed ratio, along with Tesla’s market cap of more than $1 trillion, explains much of the increase in the EV/IC ratio for the industry. (The ratio would be even higher if Rivian, which went public after November 1, 2021, was included in the sample.)

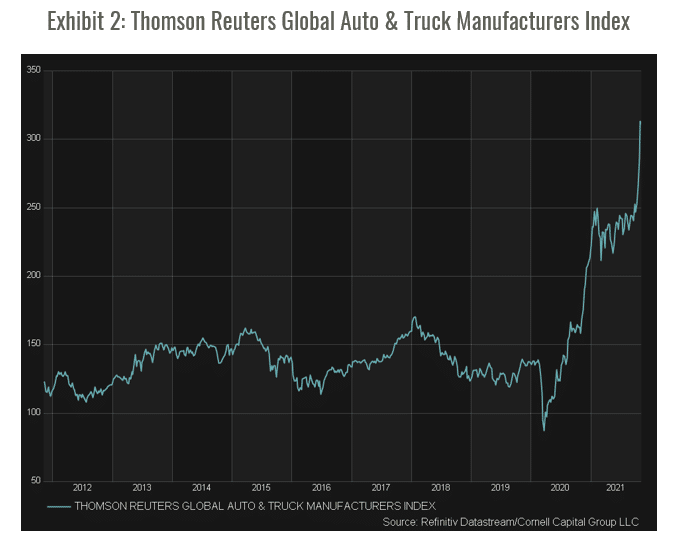

Further insight into the role played by electric vehicle specialists can be gained by examining the long-run performance of market capitalization for the industry. Exhibit 2 plots the Thompson Reuters Global Auto & Truck Manufacturers Market Capitalization index from November 2011 to November 2021. From November 2011 through the onset of Covid, the index bounces around the average level with no noticeable trend. This is consistent with the view that the market capitalization was simply tracking invested capital with little in the way of value creation. However, following the Covid market bottom the index takes off and rises almost four-fold, an increase unprecedented from the perspective of the preceding decade. That increase is due almost entirely to three factors. First, the appreciation in value of pre-existing electric vehicle specialists, primarily Tesla. Second, the entrance of new, highly valued, electric vehicle specialists such as Nio, XPeng, and Lucid. Third, appreciation in the stock prices of traditional manufacturers based on their stated plans for the future production of electric vehicles. In short, the stock market is saying that value creation in the automotive industry is almost entirely associated with the actual or proposed manufacture of electric vehicles.

The foregoing raises the question why is virtually all the recent value creation in the automotive industry is associated with switching from gas combustion propulsion to electric propulsion? From the beginning, it was known that electric cars had four fundamental advantages over internal combustion vehicles. First, 90% of electrical energy can be converted to kinetic energy of the car, whereas only about 25% of the energy stored in gasoline can be converted to kinetic energy. Second, the kinetic energy of an electric car can be converted back to electrical energy by regenerative braking, whereas all the kinetic energy is lost to heat in the brakes of fossil fuel powered vehicles. Third, electric motors require less maintenance and lubrication than internal combustion engines. Fourth, if electricity is generated by clean sources, then electric vehicles have the added benefit that they produce no pollution.

Until recently, however, the foregoing benefits were outweighed by the difficulty of storing electrical energy. Batteries were so heavy and expensive that electric cars and trucks were not practical. The key innovation that changed the industry dynamic was the invention of light weight, high energy density, lithium-ion batteries. As battery production technology improved and the cost of batteries dropped, the playing field began to tilt in favor of electric vehicles – a trend almost certain to accelerate in the future as batteries continue to improve and governments become more focused on reducing emissions of greenhouse gases.

But as epitomized by the airline industry and the auto industry prior to the electric revolution, value creation does not depend on technology – it depends on barriers to entry in deploying technology. If an industry remains capital intensive and highly competitive, then rates of return will eventually be driven down close to the cost of capital and the value of most, if not all, firms in the industry will approach the amount of the invested capital. Viewed in this light, there is no reason why transition to electric propulsion should change the valuation dynamics of the auto industry. If anything, the electric revolution has led to increased competition in the industry. The major traditional manufacturers, most of which are still around, are now facing competition from a host of electric vehicle specialists including, of course, Tesla. Furthermore, the electric car explosion has gone global with entrants from companies around the world, particularly China. As this report was in preparation, Apple announced an acceleration of its electric vehicles plans with the hope of developing fully self-driving cars within four years. In short, competition in the auto industry has been rising, and is continuing to increase, rather than declining. The influx of new companies calls to mind the early stages of the industry in the 1920s.

One explanation some analysts have offered for sky high EV/IC ratios of electric vehicle manufacturers is that the companies, particularly Tesla, do more than make cars – they are also software companies. For example, ARK Invest fund manager Cathie Wood has argued that Tesla is on the way to becoming an artificial intelligence, ride sharing, and robotics company. There are two problems with this hypothesis. The first is that there is no reason to believe that incorporating automotive software, such as self-driving capabilities, is likely to be any less competitive building cars. In fact, it opens the door to competition from trillion-dollar tech giants such as Google (Waymo), Amazon (Zoox), and Nvidia playing a role in the auto industry in addition to recent accelerated role of Apple mentioned above. Second, improved software could lead to more intensive use of vehicles as consumers gravitate toward robotaxis and forego having expensive cars sitting idle in the garage much of the time. Consequently, it is quite possible, if not likely, that improvements in self-driving technology will lead to lower vehicles sales compared to a world in which the technology was not available.

Another offered explanation is that electric car makers deserve premium valuations because they will play an important role in the transition to renewable energy and the related battle against climate change. Although it is true that electric cars are cleaner and more efficient and thereby should help reduce emissions of greenhouse gases, these are benefits that accrue to consumers and society at large, not auto manufacturers. If the industry remains highly competitive, then there is no reason that individual companies should earn rates of return much in excess of the cost of capital just because the product they make provides substantial benefits to consumers and society. Again, the air travel business is instructive. Air travel has provided huge benefits to consumers, but it has not turned airline investors into billionaires. As long as the auto industry remains highly competitive, industry EV/IC ratios should fall back to historical levels. In the short run, however, the decline may be delayed by government subsidies for electric vehicles designed to promote use of clean energy. But these subsidies also encourage further entry into the market, particularly if there are limits on the number of cars per producer that qualify for the subsidy. Furthermore, in the longer run these subsidies will also be captured by consumers if competition drives down the prices of electric cars.

In the short run, electric car manufacturers have also benefitted from the current ESG investing boom. Elon Musk has been particularly effective in beating the drum for the environmental benefits of electric cars. But investor enthusiasm also attracts new entrants and encourages them to go public as quickly as possible, via a SPAC if necessary, to share in the torrents of investor cash. The financial incentives to enter quickly further increase competition in the industry making it more difficult for competing companies to earn rates in excess of the cost of capital in the long run.

Even if EV/IC ratios fall back toward 1.0 for most all companies in the industry, it is possible that a few dominate firms will emerge and account for most all the value creation analogous to Amazon in online retail. For those firms, EV/IC ratios could remain substantially above 1.0. Tesla is a prime candidate here. Currently, the company has two fundamental advantages compared to other auto manufacturers. The first is profitability. Due to its operating cost structure, unconventional distribution model (which bypasses dealerships), and its ability to increase revenues by selling related products and services, Tesla has an opening to deliver higher margins than other automobile companies. The second is related to Tesla’s investment and capital intensity. Tesla has avoided building large and expensive assembly plants ahead of time. As a result, the company has been able to scale up more quickly while reinvesting less in capacity than its traditional competitors. The problem with both these advantages is that they likely to be ephemeral, particularly compared to new entrants. Both Lucid, and now public Rivian, are essentially copying Tesla’s model and Apple certain could as well. It should also be possible for traditional manufacturers to move in that direction.

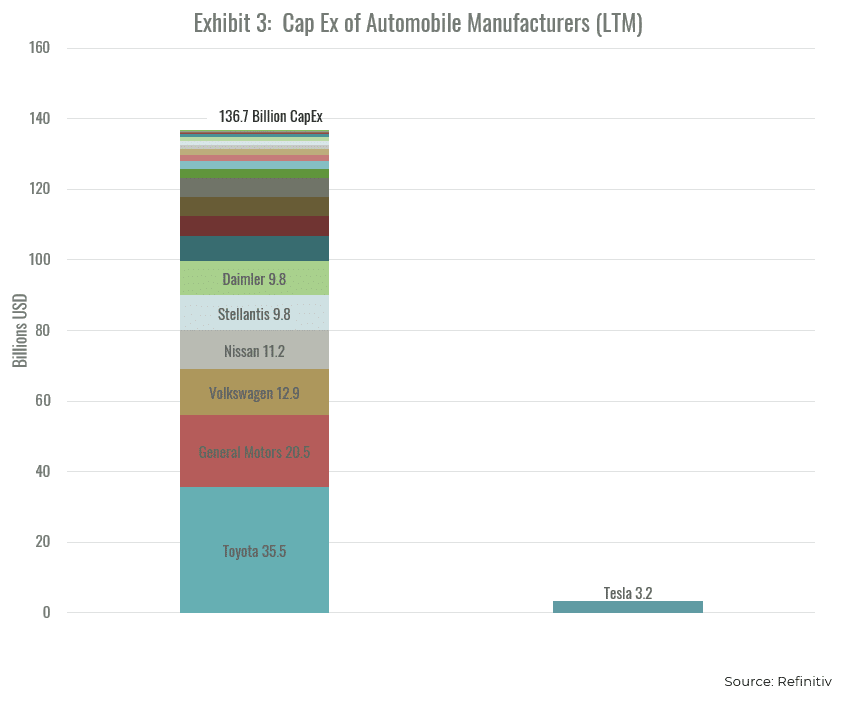

One way to investigate the likelihood of a dominant firm or two emerging is by looking at the capital expenditures of competing companies. Presumably developing new technologies sufficient to dominant numerous competitors will not come cheaply. The key items are research and development and capital expenditures. Unfortunately, not all auto manufacturers break out research and development. Exhibit 3 plots the capital expenditures for major auto makers. Somewhat surprisingly, Tesla is not near the top of the list. In fact, it ranks behind seven of the traditional manufacturers. With regard to research and development, Tesla reported $1.49 billion for 2020. In comparison, NASDAQ reports that research and development expenditures in 2020 were $16.5 billion for VW, $10.2 Daimler, $9.9 for Toyota, $7.1 for Ford and $6.2 for GM. Given the importance of research and development and capital expenditures, the foregoing provides no reason to believe that Tesla is imminently going to become a dominant manufacturer. It is difficult to see how Tesla could increase its market capitalization gap, relative to its major competitors, given its smaller R&D and capital expenditures. In addition, Tesla plans to grow much more rapidly than its competitors and that will require added investment. Furthermore, Chinese companies are likely to have access to government financial support for research and new investment as they move to supplant Tesla in China, the world’s largest automobile market. Finally, the entrance of Apple with its huge cash hoard and technological prowess should be a large impediment to Tesla becoming dominant company.

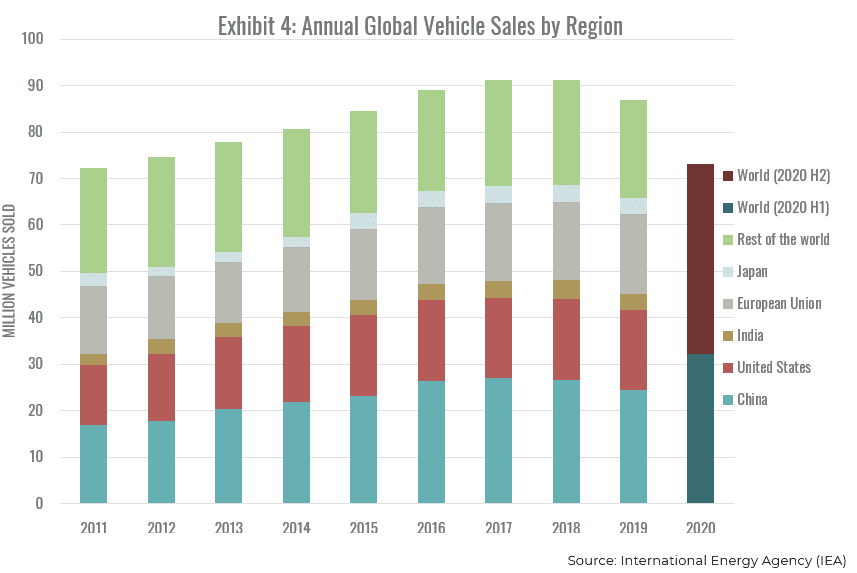

Playing devil’s advocate, if Tesla were going to become a dominant firm, as stock market seems to be saying based on its massive market capitalization, then that should be bad news for its competition unless the industry is exploding in the way that online video streaming did. That, however, is not the situation in the case of automobiles and light trucks. Exhibit 4 plots annual global unit auto sales from 2011 through 2020. Regional data is shown through 2019. In 2020 regional data is no longer available and the sample is divided into the first half and second half of the year.

The exhibit reveals that growth in auto sales has basically mirrored growth in the overall world economy. Furthermore, most of the global sales growth was due to China which was undergoing dramatic economic expansion during the decade. Going forward, there is no reason to believe that growth in sales of autos and light trucks will exceed growth in global real GDP. In fact, as noted earlier, technological innovations such as self-driving, may make for more intensive use of vehicles and retard growth in unit sales.

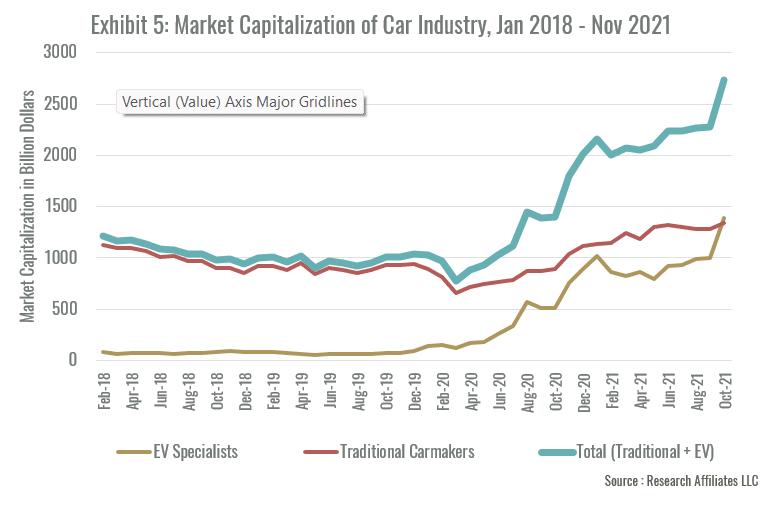

The industry sales data flies in the face of stock market performance. Not only has Tesla risen to become the fifth most valuable company in the world as measured by market capitalization, but the stock price of any company that has anything to do with electric vehicles has risen right along with it. As evidence, Exhibit 5 provides a close-up showing the recent appreciation in the market capitalization of the car industry during the period from January 2018 through November 2021. The exhibit does not include Rivian which would add more than $100 billion to the overall industry capitalization and to the EV specialists. Although most of the increase in industry value is due to EV specialists, the stock price of virtually every individual auto manufacturer rose reflecting stock market’s view that the transition to electric cars will lead to massive value creation throughout the industry despite slow growth in total unit auto sales.

In our opinion, current stock market valuations are a prime example of what Cornell and Damodaran (2020) call the “the big market delusion.” As Arnott, Wu, and Cornell (2021) observe, the hallmark of a big market delusion is when all the firms in an evolving industry rise together even when they are direct competitors. Investors become so enthusiastic that each firm is priced as if it will be a major winner in the involving big market despite the fact this is a fallacy of composition; the sum of the parts cannot be great than the whole.

Investment Implications

The analysis presented here implies that the transition to electric vehicles will not fundamentally change the nature of the automotive industry. Although electric cars will become predominant, the industry will remain highly competitive and capital intensive. If anything, the electric vehicle boom has made the market even more competitive as electric vehicles specialists enter to compete with traditional manufacturers.

Because we believe that the competitive structure of the market will remain unchanged, it is our view that in the long run EV/IC ratios will regress toward their historical average of about 1.10, primarily due to the stagnation or outright decline in the stock prices of auto manufacturers. The higher the current EV/IC ratio, the more likely the stagnation or decline. Over the next decade, it will be difficult for investors in auto manufacturers to earn meaningfully positive stock returns with the outlook for investment in electric vehicle specialists being particularly bleak. However, along the way there are likely to be bouts of momentum and sentiment from which traders might try to profit. Nonetheless, we agree with Benjamin Graham when he observed in the short run the market is a voting mechanism, but in the long run it is a weighing mechanism.

References

Arnott, Rob, Bradford Cornell and Lillian Wu, 2021, Big market delusion: Electric vehicles, Research Affiliates, March, 1-9.

Cornell, Bradford and Aswath Damodaran, 2020, Big market delusion: Valuation and investment implications, Financial Analysts Journal, 76, 2, 15-25.